MARKETS TODAY August 16th, 2023 (Vica Partners)

Overnight/US Premarket, Asian markets finished lower, Japan’s Nikkei 225 lost 1.46%, the Hong Kong’s Hang Seng was down 1.36% and China’s Shanghai Composite was off 0.82%. S&P futures opened trading at 0.09% below fair value.

European markets finished mixed, Germany’s DAX gained 0.18% while London’s FTSE 100 lost 0.44% and France’s CAC 40 down 0.10%.

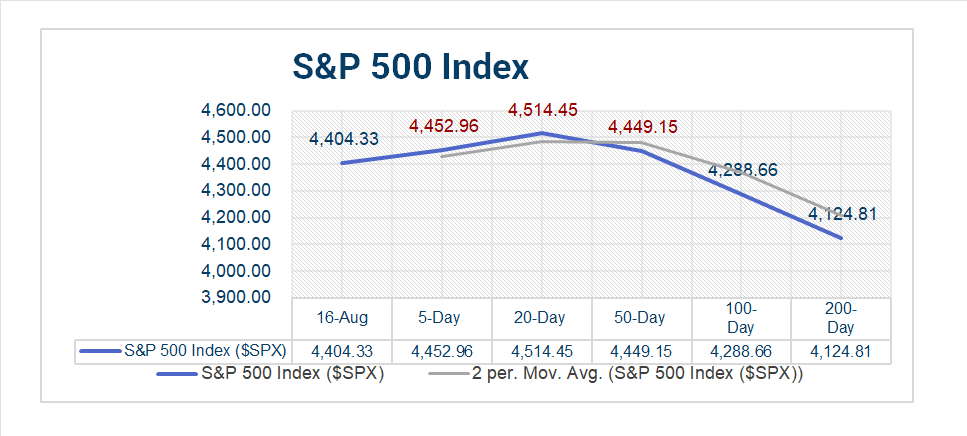

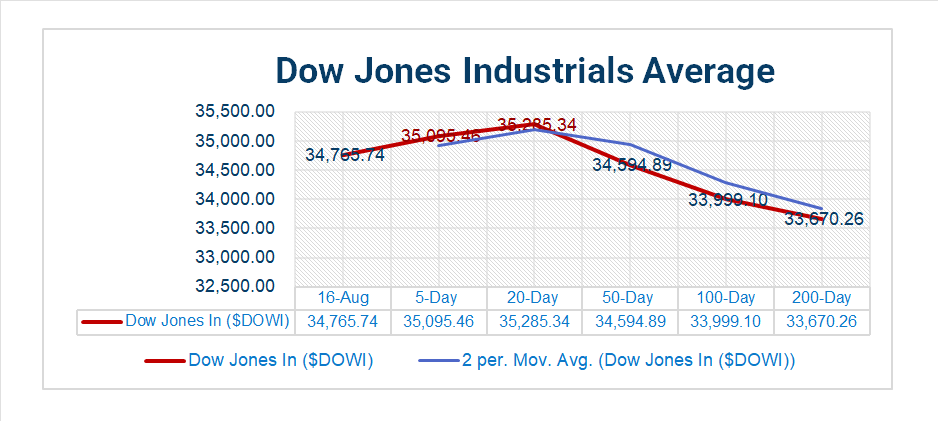

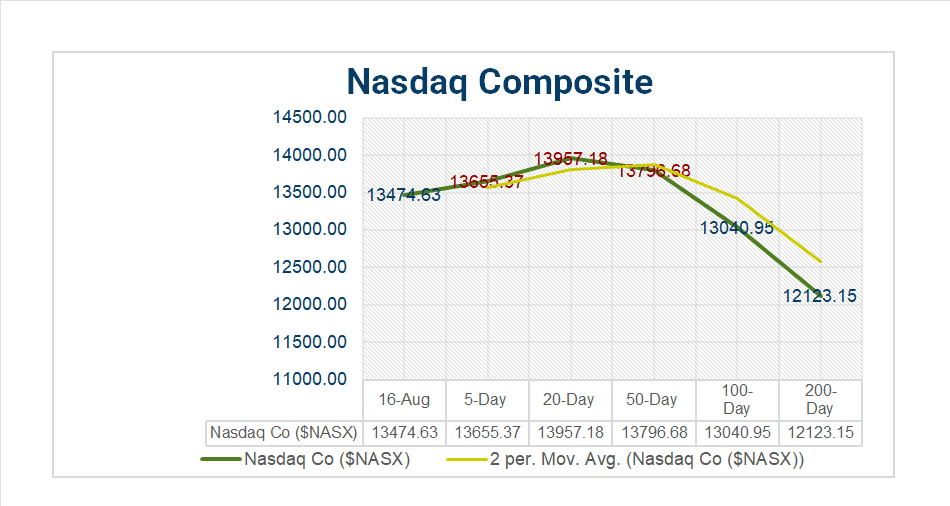

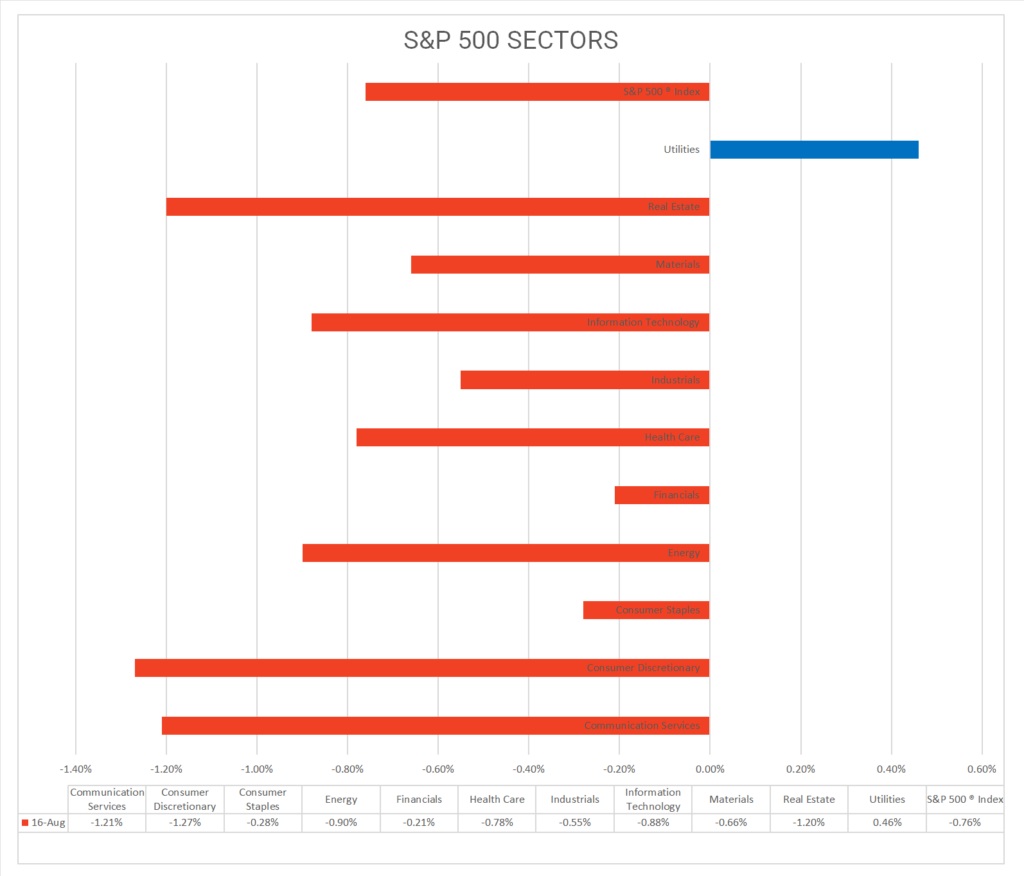

Today US Markets finished lower, the NASDAQ lost 1.15% the S&P 500 down 0.76% and the DOW off 0.52%. 10 of 11 S&P 500 sectors declining: Utilities +0.46% outperforms/ Consumer Discretionary -1.27% lags. On the upside, Industries: Independent Power and Renewable Electricity Producers, Insurance, Gas and Multi Utilities ProShares UShort 20+ Treas ^TBT, US Treasuries, USD Index.

In US economic news, US housing starts in line and building permits missed consensus. Production and manufacturing came in ahead of estimates while capacity utilization improved. Fed’s July meeting minutes signaled officials are aware of the risks of overtightening however remain on focused on 2% inflation target.

Takeaways

- US production and manufacturing came in ahead of estimates

- All three of the major U.S indexes decline

- 10 of 11 S&P 500 sectors declining: Utilities +0.46% outperforms/ Consumer Discretionary -1.27% lags.

- Trending Industries: Independent Power and Renewable Electricity Producers +2.28%, Insurance +1.37%, Gas Utilities +0.84%, Multi-Utilities +0.84%

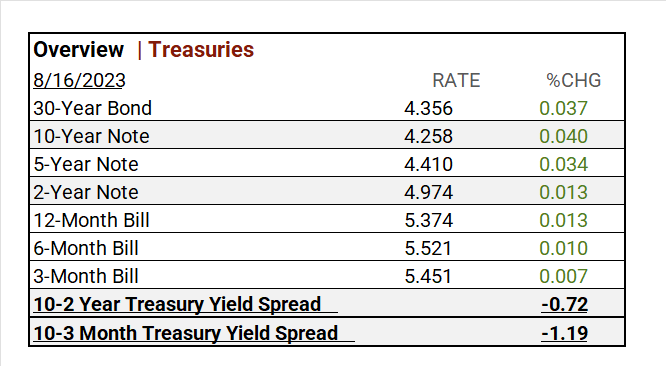

- US Treasury yields up across the curve

- ProShares UShort 20+ Treas ^TBT +1.50%

- USD Index gains

- Progressive (PGR) +8.8% was the S&P 500 top performer

- TJX (TJX) with solid earnings beat

- Options expiration end of week

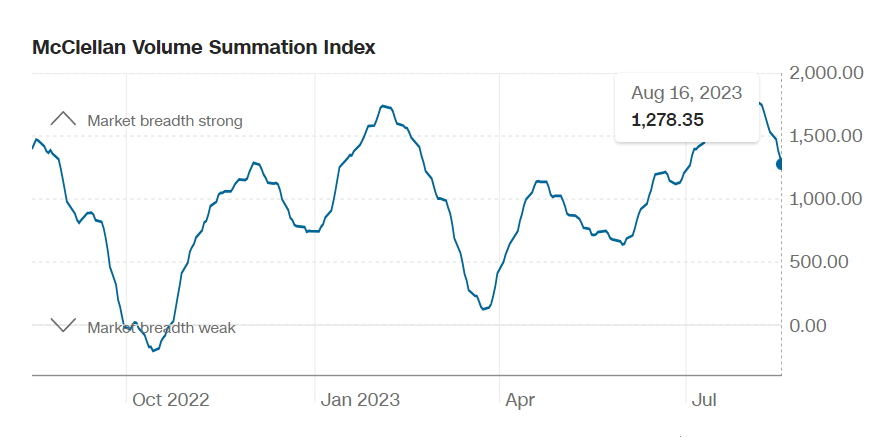

Pro Tip: The McClellan Volume Summation measures the volume, of shares on the NYSE that are rising compared to the number of shares that are falling.

Sectors/ Commodities/ Treasuries

Key Indexes (5d, 20d, 50d, 100d, 200d)

S&P Sectors

- 10 of 11 S&P 500 sectors declining: Utilities +0.46% outperforms/ Consumer Discretionary -1.27% lags.

- Industries: Independent Power and Renewable Electricity Producers +2.28%, Insurance +1.37%, Gas Utilities +0.84%, Multi-Utilities +0.84%

- *1 Month Leaders: Energy +7.19%, Health Care +2.87%, Communication Services +1.02%

- *YTD Leaders: Communication Services +41.11%, Information Technology +36.83%, Consumer Discretionary +31.82%

- *S&P 500 +15.58% *as of Aug-15-2023

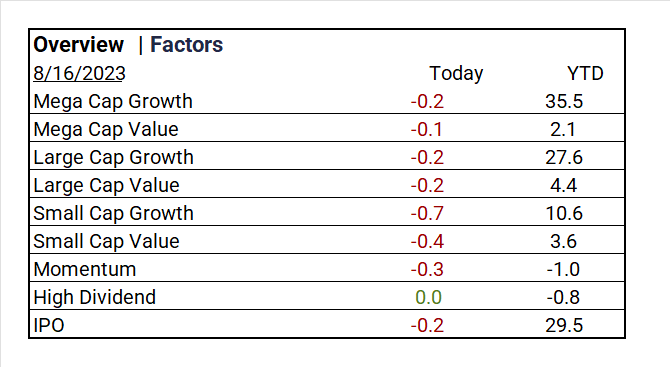

Factors

US Treasuries

US Treasuries

Earnings

Q2 ’23 Top Line Top Line

- Q1 ’23 Actual: 79% of companies beat analyst estimates by an average of 6.5%

- Q2 Forecast: S&P 500 EPS was expected to decline <7.2%>/ Fiscal year 2023 EPS flat YoY

Q2 Actual (TBA)

Notable Earnings Today

- +Beat: Cisco (CSCO), TJX (TJX), Synopsys (SNPS), JD.com Inc Adr (JD), Coherent (COHR), Brinker (EAT), Amcor PLC (AMCR), StoneCo (STNE), Avnet (AVT), Paycor HCM (PYCR), Navigator Holdings (NVGS)

- – Miss: Tencent ADR (TCEHY), Target (TGT), Hong Kong Exchange & Clearing (HKXCY), Performance Food Group Co (PFGC), ZIM Integrated Shipping Services (ZIM), Dada Nexus (DADA)

Economic Data

US

- Housing starts July: act 1.45m, fc 1.45m, prior 1.40m

- Building permits July: act 1.44m, fc 1.47m, prior 1.44m

- Industrial production July: act 1.0%, fc 0.5%. prior -0.8%

- Capacity utilization July: act 79.3%, fc 79.1%, prior 76.8%

Vica Partner Guidance August ’23, (updated 8-16)

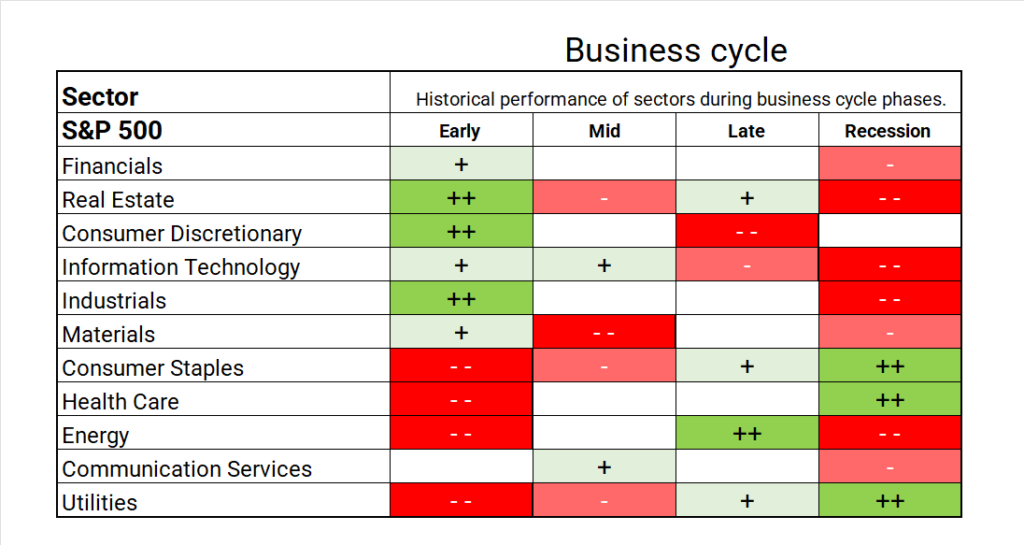

- Q3+/4 highlighting: Energy sector trending in current late business cycle. Industries; Energy Equipment & Services, Oil, Gas & Consumable Fuels, Interactive Media & Services, Construction Materials, Media, Broadline Retail, Health Care Providers & Services, Containers & Packaging, Office REITs, Ground Transportation, Communications Equipment, Machinery Biotechnology, Pharmaceuticals, Capital Markets, Construction & Engineering, Building Products, Machinery.

- Mid Term: Q4 sector shift to Utilities and Health Care. Slight regression on Semiconductor & Semiconductor. Specialized REITs have upside. Undervaluation for Chinese Mega Cap Tech. Japan equities still a better value than US. Smart money has already started investing in Real Estate/ builders for a good 18 months out.

- Cautionary: Current shorter term “hard” shift from Growth to Value. Industries: Independent Power and Renewable Electricity Producers, Automobiles, Automobile Components, Consumer Finance, Passenger Airlines, Hotel & Resort REITs. Materials on China deflation. Credit default swap (CDS) to pick-up through Q4/Q1. >20 Year Treasuries price erosion.

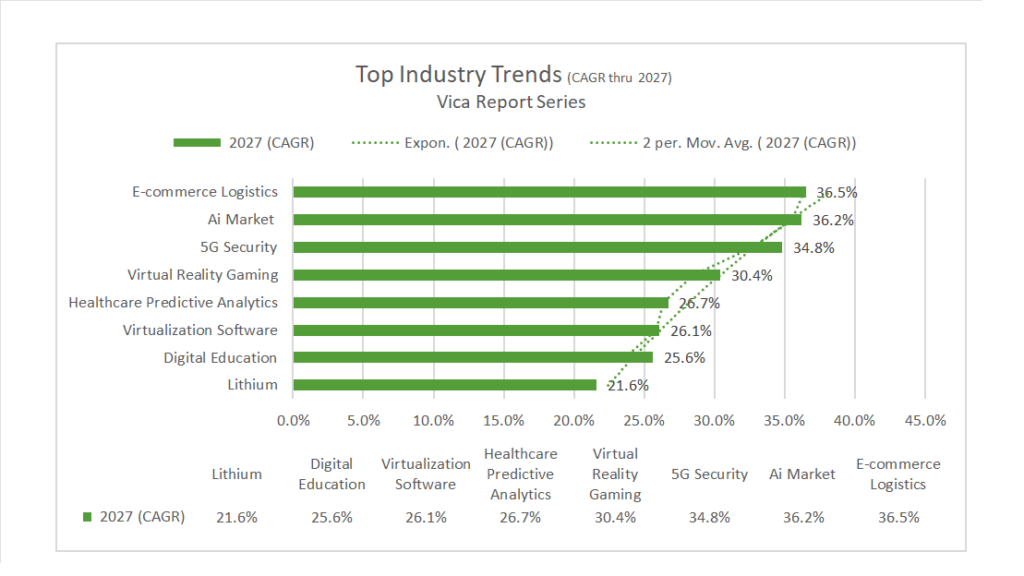

- Longer Term: NASDAQ 100^NDX/FANG+ ^NYFANG companies will continue to outperform “BIG allows you to invest at scale”. TOP Sector outperform includes AI and Semiconductor Equipment, Key materials like Lithium and Uranium. Forward looking CAGR growth below:

- Company: we continue to emphasize longer term business strength *quality and strength of balance sheet for all investments. * Strong Mega Cap longer support – NVIDIA (NVDA), Meta Platforms (META), Microsoft (MSFT), Alphabet (GOOG, GOOGL), Amazon (AMZN), Apple (AAPL), Tesla (TSLA), Taiwan Semi (TSM), ASML Holding NV (ASML).

- BIG Picture: Market bottoms are made on bad news and with deflationary signals the current market rally should come as no surprise. The combination of current Fed tightening, higher oil prices and a strong dollar should have given us a final bottom in ’23?

- Our biggest concern with the current rally is that the Government is not as effective as Free Markets in managing capital. Stock repurchases are just another way to deploy Capital. Consider that about 63% of the typical business cost is labor. I wholeheartedly trust the Free Market to better spend on CAPEX, R&D, and other.

- As for Bonds as an alternative investment for Stocks, a >10-year bond should have a return that exceeds nominal GDP, assuming inflation remains above >3%.

- The argument for Fed further tightening has its pundits. Raising rates to counter jobs (1.6 jobs available for every job seeker) in a rapidly changing economy will NOT moderate on demands.

- The Fed would benefit by rethinking its 2% inflation target and adjusting it to 3%. This would account for more accurate wages, energy transitions and account for expanding services in BIG tech. In addition, add more protection from deflation.

News

Company News/ Other

- Aldi to Buy Winn-Dixie Supermarket Owner in US Southeast Expansion – Bloomberg

- Estée Lauder’s Big Bet on China Is Looking Not So Pretty – WSJ

Energy/ Materials

- A Year Into Biden’s Climate Agenda, the Price Tag Remains Mysterious – Bloomberg

Real Estate

- A Real-Estate Haven Turns Perilous With Roughly $1 Trillion Coming Due – WSJ

Central Banks/Inflation/Labor Market

- Fed Saw ‘Significant’ Inflation Risk That May Merit More Hikes – Bloomberg

- Russia’s Central Bank Can’t Stop Ruble Trouble – WSJ

Asia/ China

- Xi Jinping speech calling for patience released amid economic gloom – South China Morning Post