MARKETS TODAY August 9th, 2023 (Vica Partners)

Overnight/US Premarket, Asian markets finished mixed, Hong Kong’s Hang Seng gained 0.32%, Japan’s Nikkei 225 lost 0.53% and China’s Shanghai Composite down 0.49%. S&P futures opened trading at 0.05% above fair value.

European markets finished higher, London’s FTSE 100 gained 0.80%, France’s CAC 40 up 0.72% and Germany’s DAX up 0.49%.

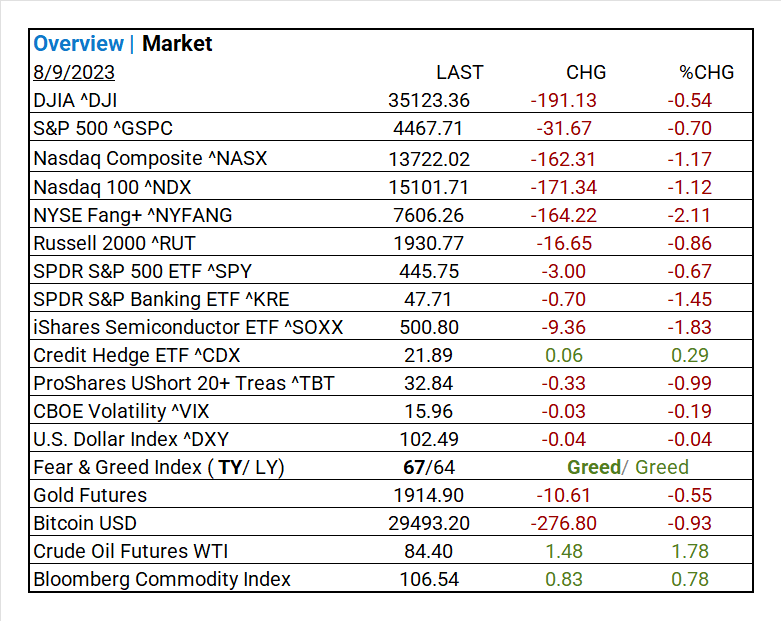

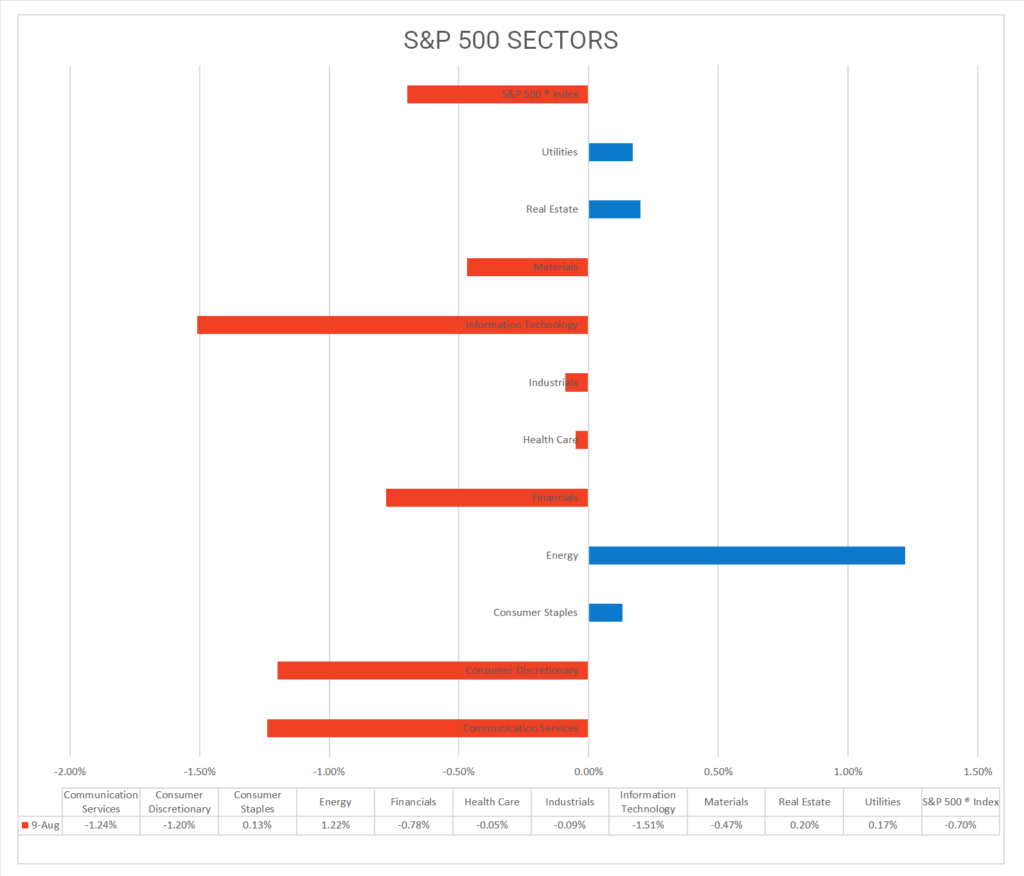

Today US Markets finished lower, the S&P 500 was off 0.70%, the DOW down 0.54% and the NASDAQ lost 1.17%. 7 of 11 S&P 500 sectors declining: Energy +1.22% outperforms/ Information Technology -1.51% lags. On the upside, Credit Hedge ETF ^CDX, Industries: Energy Equipment & Services, Oil, Gas & Consumable Fuels, Wireless Telecommunication Services, Oil and Bloomberg Commodity Index.

In US economic news, no major releases today however MBA Mortgage data for the week ending August 4 showed a 3.1% decline in mortgage applications.

Takeaways

- China’s entering deflation

- 7 of 11 S&P 500 sectors declining: Energy +1.22% outperforms/ Information Technology -1.51% lags.

- Industries: Energy Equipment & Services +1.61%, Oil, Gas & Consumable Fuels+1.18%, Wireless Telecommunication Services +1.06%

- Credit Hedge ETF ^CDX up

- Oil and Bloomberg Commodity Index gain

- Vistra Energy (VST) Reynolds (REYN) w/ solid pre-market earning beats

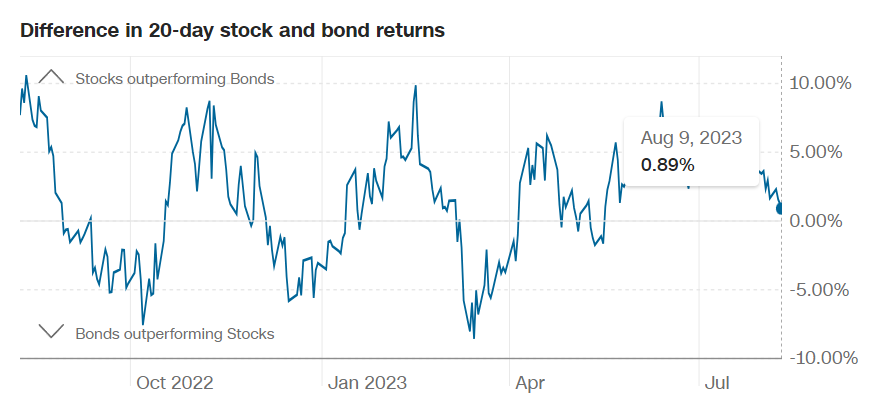

Pro Tip: Safe Haven Demand shows the difference between Treasury bond and stock returns over the past 20 trading days. The current rating indicates market increased volatility.

Sectors/ Commodities/ Treasuries

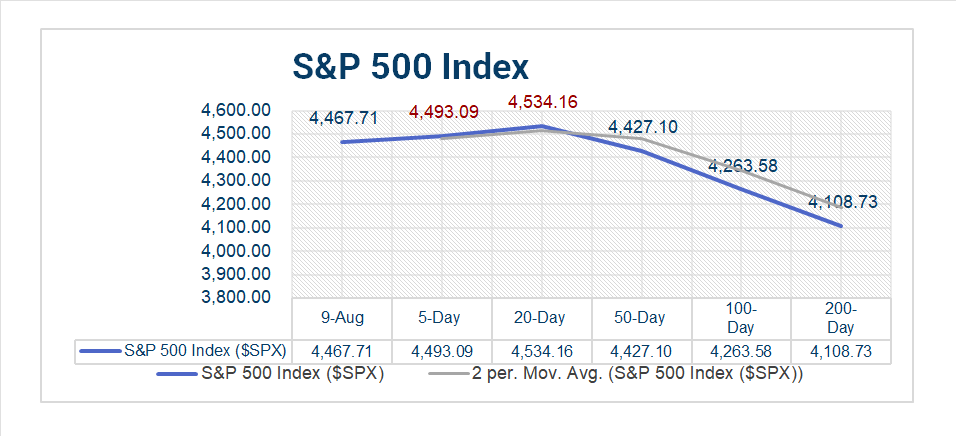

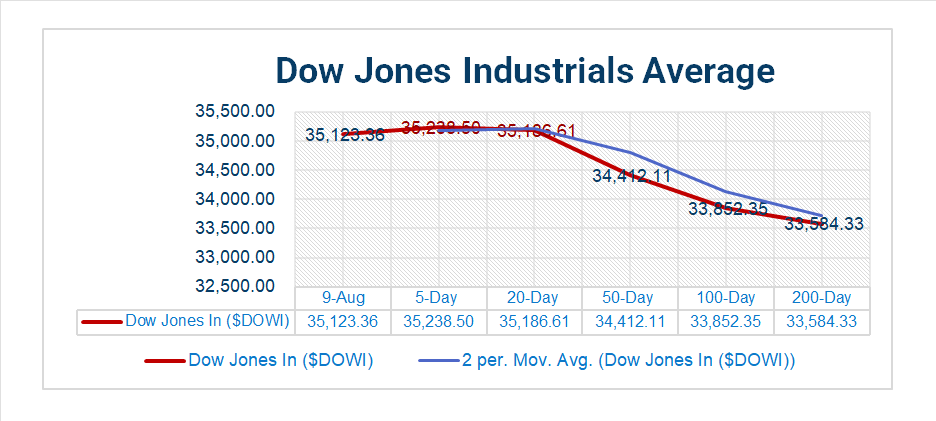

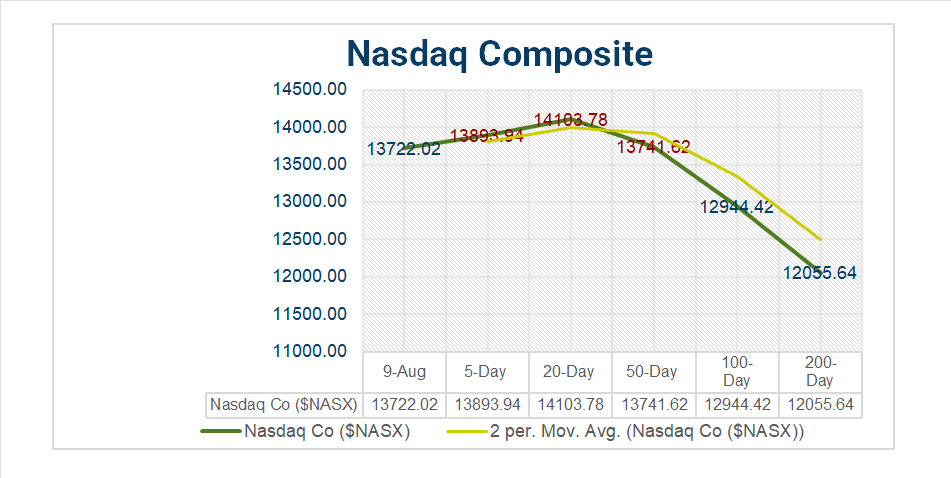

Key Indexes (5d, 20d, 50d, 100d, 200d)

S&P Sectors

- 7 of 11 S&P 500 sectors declining: Energy +1.22% outperforms/ Information Technology -1.51% lags.

- Industries: Energy Equipment & Services +1.61%, Oil, Gas & Consumable Fuels+1.18%, Wireless Telecommunication Services +1.06%, Specialized REITs +0.80%

- MTD Leaders: Energy +7.78%, Communication Services +5.77%, Health Care +4.50%

- YTD Leaders: %, Communication Services +42.95%, Information Technology +38.87%, Consumer Discretionary +34.75%

- S&P 500 +17.19%

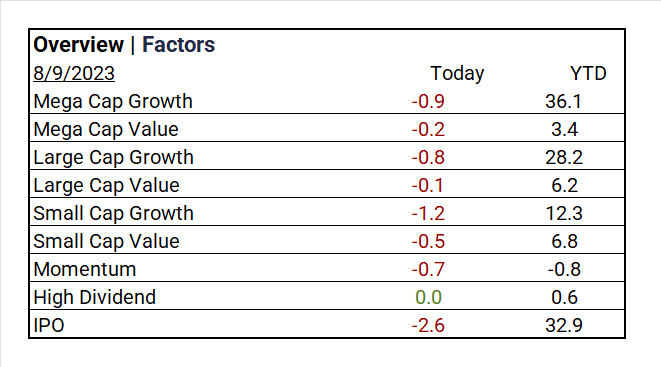

Factors

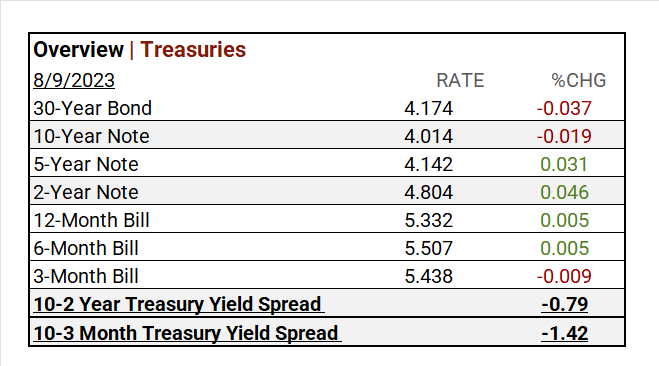

US Treasuries

US Treasuries

Earnings

Q2 ’23 Top Line Top Line

- Q1 ’23 Actual: 79% of companies beat analyst estimates by an average of 6.5%

- Q2 Forecast: S&P 500 EPS was expected to decline <7.2%>/ Fiscal year 2023 EPS flat YoY

Q2 Actual (thru 8/04)

- 84% of the S&P 500 have reported results for the second quarter of 2023

- Companies represented in the Morningstar US Market Index are expected to see their earnings decline by about 5.27% from a year ago.

- Based on earnings consensus estimates, consumer cyclical companies are forecast to see the most growth, followed by energy, industrials, and financial services.

Notable Earnings Today

- +Beat: Sony ADR (SONY), The Trade Desk (TTD), Illumina (ILMN), Hannover Re (HVRRY), Wynn Resorts (WYNN), Vistra Energy (VST), Charles River Laboratories (CRL), Applovin (APP), Tetra Tech (TTEK), CAE Inc. (CAE), Valvoline (VVV), Reynolds (REYN)

- – Miss: Walt Disney (DIS), Nippon ADR (NTTYY), Honda Motor ADR (HMC), EON SE (EONGY), Bridgestone ADR (BRDCY), Vestas Wind (VWSYF), Terumo ADR (TRUMY), FUJIFILM Holdings Corp (FUJIY), Roblox (RBLX), U-Haul Holding (UHAL), Isuzu Motors (ISUZY), Roblox (RBLX)

Economic Data

US

- No major releases scheduled.

Vica Partner Guidance August ’23, (updated 8-09)

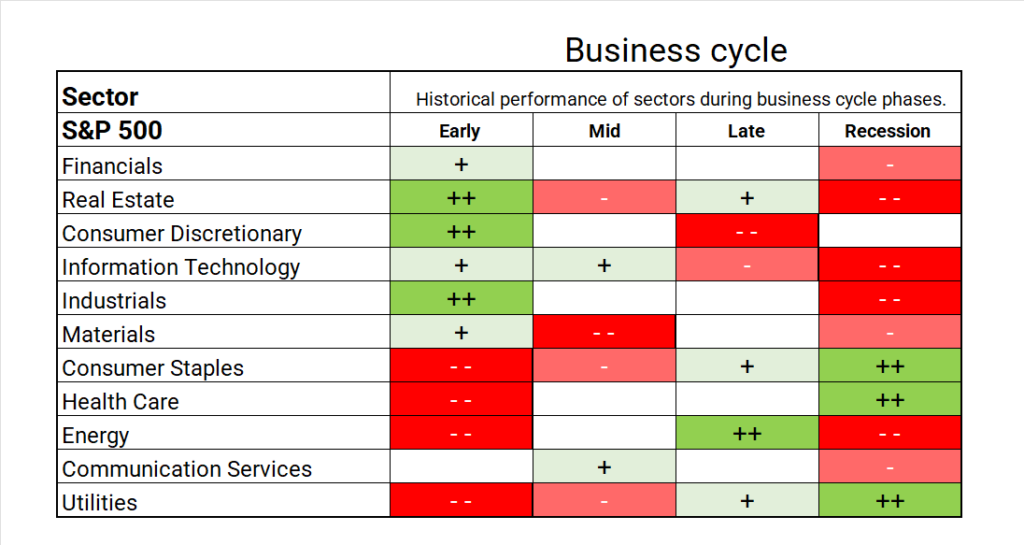

- Q3/4 highlighting, Industries: Interactive Media & Services, Household Durables, Broadline Retail, Consumer Finance, Automobiles, Construction & Engineering, Semiconductor & Semiconductor Equipment, Energy Equipment & Services, Construction Materials, Specialized REITs, Gas Utilities. Other: Undervaluation for Chinese Mega Cap Tech. Japan equities still a better value than US. Look for continued strength in Mega and Large Cap Growth “the new defensives” Expect Energy Sector rally!

- Cautionary, Banks shortly may be overpricing. Current indicators are mixed. Credit default swap (CDS) to pick-up through Q4/Q1. >20 Year Treasuries price erosion.

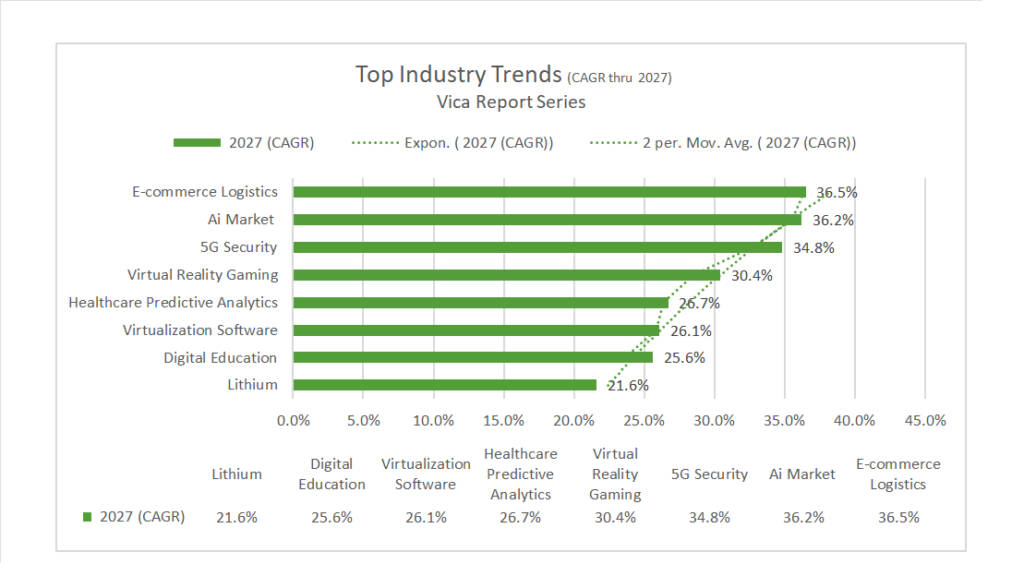

- Longer Term, NASDAQ 100^NDX/FANG+ ^NYFANG companies will continue to outperform “BIG allows you to invest at scale”. TOP Sector outperform includes AI and Semiconductor Equipment, Key Material like Lithium. Forward looking CAGR growth below:

- Company, we continue to emphasize business *quality and strength of balance sheet for all investments. * Strong support – NVIDIA (NVDA), Meta Platforms (META), Microsoft (MSFT), Alphabet (GOOG, GOOGL), Amazon (AMZN), Apple (AAPL), Tesla (TSLA), Taiwan Semi (TSM), ASML Holding NV (ASML), Broadcom (AVGO).

- BIG Picture: Market bottoms are made on bad news and with deflationary signals the current market rally should come as no surprise. The combination of current Fed tightening, higher oil prices and a strong dollar should have given us a final bottom in ’23?

- Our biggest concern with the current rally is that the Government is not as effective as Free Markets in managing capital. Stock repurchases are just another way to deploy Capital. Consider that about 63% of the typical business cost is labor. I wholeheartedly trust the Free Market to better spend on CAPEX, R&D, and other.

- As for Bonds as an alternative investment for Stocks, a >10-year bond should have a return that exceeds nominal GDP, assuming inflation remains above >3%.

- The argument for Fed further tightening has its pundits. Raising rates to counter jobs (1.6 jobs available for every job seeker) in a rapidly changing economy will NOT moderate on demands.

- The Fed would benefit by rethinking its 2% inflation target and adjusting it to 3%. This would account for more accurate wages, energy transitions and more BIG tech market-based institutions. In addition, add more protection from deflation.

News

Company News/ Other

- Banks’ Problems Aren’t Over, According to the Bond Market – WSJ

- Citadel Securities Boosts Fixed-Income Presence With New Bond Trade – Bloomberg

- Disney to Significantly Raise Prices of Disney+, Hulu Streaming Service – WSJ

Energy/ Materials

- Three Trends to Watch in Electric-Vehicle Charging – Bloomberg

- Oil Hits High for the Year as Supply Risks Grow in Tight Market – Bloomberg

Central Banks/Inflation/Labor Market

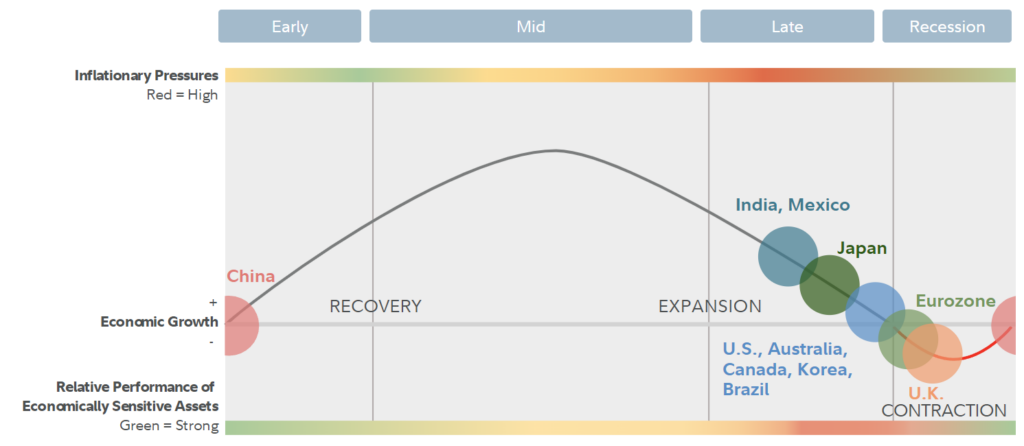

- China Slips Into Deflation in Warning Sign for World Economy – WSJ

Asia/ China

- Biden plans new restrictions on US investments in China, declares ‘emergency’ on sensitive tech – South China Morning Post