Liquidity Is Holding the Line While Pricing in a Scare, Not a Break.

Abstract

Markets behaved this week as though something fundamental had cracked — but the system itself did not. Sentiment collapsed into Extreme Fear, breadth deteriorated to its weakest level since early summer, and safe-haven demand strengthened in a pattern that typically precedes volatility repricing. Yet none of the structural components that define genuine breakdown — liquidity torque failure, credit deterioration, or instability in volatility transmission — actually materialized.

What we’re seeing is a psychological disruption, not a structural one. Liquidity corridors in AI infrastructure, megacap balance-sheet strength, and quality-carry sectors continue to anchor the system. Credit spreads widened, but remained inside critical thresholds. Volatility correlations shifted defensive, but stayed orderly. And the VMSI composite — the market’s inertia field — held firmly above equilibrium at 57.8, signaling elevated stress but nowhere near systemic fracture.

This divergence between fear in price and stability in structure is the hallmark of late-equilibrium markets. Surface psychology becomes erratic. Narrative volatility accelerates. But the underlying mechanics — liquidity, torque symmetry, credit elasticity — remain intact. Historically, this is the regime that produces asymmetric opportunity for allocators who understand that panic is external while stability is internal.

The market is not signaling collapse. It is signaling containment. And in containment regimes, protection becomes overpriced while persistence becomes undervalued — a setup where disciplined structure consistently outperforms emotion.

1. Weekly Summary — Week Ending November 21, 2025

Fear is accelerating faster than risk — but the system’s internal architecture continues to hold.

This was the first week since August in which investor psychology fully detached from structural reality. Sentiment collapsed into Extreme Fear (CNN F&G: 11), breadth fell to its weakest point since early Q2, and safe-haven demand moved into levels normally seen before volatility repricing events. At the surface, the narrative is one of fragility.

But the underlying system — the liquidity spine that actually governs market continuity — remained stable.

Liquidity (58.1) stayed well above the continuity floor, and execution capacity remained firm even as breadth deteriorated. Momentum weakened to 55.3, consistent with a market losing elasticity but not losing control. Volatility & Hedging reached 60.8, a defensive alignment, yet the vol structure remained coherent: the VIX at 23.43 is elevated, but cross-asset volatility ratios indicate compression rather than contagion. This is not disorder — it is premium being paid for insurance.

Credit confirmed that fear has not yet become risk. High-yield spreads widened but remained beneath the 350 bps stress trigger — the line where liquidity stops absorbing shocks and begins transmitting them. IG spreads weakened at the margin but did not break. This is a market that anticipates stress but has not yet entered a stress regime.

The deterioration came from participation, not from structure. Small- and mid-cap liquidity decayed sharply. Dispersion narrowed. Flow in AI-linked, mega-cap, and quality balance-sheet names once again carried the majority of index torque. This is classical late-equilibrium geometry: the system becomes narrower, more selective, and more energy-intensive, yet the primary liquidity corridors continue to function as the backbone.

ETF flow and sector behavior validated this narrowing:

-

Growth/AI megacaps retained structural dominance.

-

JAVA (Active Value) showed resilient balance but declining trend energy.

-

SOXX and related semis kept their liquidity corridors intact, though torque decay increased.

-

GDX strength (+0.9%) confirmed quality-duration hedging flows.

-

LQD remained structurally stable; HYG drifted outward but stayed contained.

This is not a market breaking — it is a market reallocating under duress.

Macro data remained consistent with softening, not failure. Retail sales slipped, core goods demand cooled, durable orders softened, and consumer confidence edged lower. Shutdown distortions still contaminate the signal, but Q4 tracking is still in the “slowing, not collapsing” band. Inflation expectations ticked modestly higher, labor loosened at the edges, and leading indicators remain recession-adjacent — reinforcing duration and quality without forcing credit repricing.

Valuation pressure is the real vulnerability. Forward multiples near 20× are being supported by a liquidity system that is becoming progressively less efficient. Every additional unit of stability now requires more liquidity torque. This setup rarely persists without either (1) a reset in credit or (2) a re-expansion in participation. Neither has occurred — meaning continuity now depends almost entirely on liquidity inertia.

Structural Conclusion: This week showcased the core late-cycle paradox: The market is terrified. The system is not.

Liquidity is thinner but functional. Credit is softer but contained. Volatility is elevated but orderly. Momentum is weaker but still supported by structural liquidity fields.

This is the definition of a high-cost stability regime — the system is working harder to stay balanced, but balance remains intact.

Bottom Line: The panic is real, but the mechanics are not breaking. The next decisive signal will come from credit and breadth:

-

HY > 350 bps or breadth < 45% on a multi-session basis → the system shifts into compression.

-

If neither breaches, this week will be remembered as another dislocation the structure absorbed — not the start of a broader unwind.

This is not optimism; it’s structural math. The system is strained — but it’s still holding the line.

2. Framing Note — FORCE-12.3 Calibration

FORCE-12.3 is built to identify the exact moment when liquidity stops creating momentum and starts manufacturing stability — the late-equilibrium regime where markets trade on continuity, not conviction.

Its torque model isolates four shifts:

-

Execution capacity stayed firm.

-

Flow amplification weakened.

-

Systemic friction increased.

-

Reflexivity rose as positioning crowded into mega-cap, AI-linked, and IG-carry corridors.

The signal for the week: Liquidity is still functional — but now defending the system rather than amplifying it.

This explains the gap between surface-level fear and underlying resilience: sentiment broke, but structural torque did not. No reflexive failure, no liquidity fracture, no transition into pre-compression.

Interpretation: The market has moved into a high-cost, tightly wound equilibrium. It is harder to break — and harder to accelerate. Stability persists, but it now requires meaningfully more liquidity per unit of order.

3. Liquidity & Torque Dynamics — The Physics Behind 57.8

At 57.8, the system sits above the stability floor, but the internal mechanics reveal a decisive shift: liquidity is no longer supporting stability — it is defending it.

Liquidity (58.1) remained functional but weaker, well below the >60 readings that powered October’s advance. Execution capacity (ECₜ ≈ 0.93) stayed firm, yet flow amplification (Fₜ) deteriorated as participation collapsed. NYSE breadth printed its weakest levels since early summer, with net highs/lows decisively negative. The energy that previously came from dispersion now comes from a narrow spine of AI-linked, mega-cap, and quality-carry liquidity corridors.

Systemic friction (μₜ) increased for a second consecutive week — not enough to impair stability, but enough to indicate that each marginal unit of liquidity now absorbs volatility rather than propelling trend. Reflexivity (ψₜ) climbed sharply as flows crowded the same high-density channels, reinforcing a market that holds motion but resists acceleration.

Volatility now confirms this shift. The VIX spiked to 23.43, with every major technical metric (ATR, Stochastics, ADX) showing heightened defensive pressure. Vol correlations tightened across assets — a classic late-equilibrium pattern — but volatility remains orderly, not disorderly. This reflects high-cost continuity: volatility is rising, but still largely suppressed by liquidity structure.

Credit torque held firm. High yield widened toward the 350 bps perimeter but did not break. IG spreads softened to 112 bps, losing their tightening impulse but not flipping into stress. That combination — wider, but contained — marks pre-compression, not failure. Credit is warning, not breaking.

Breadth deterioration completes the picture. With institutional corridors carrying nearly all index torque, and retail outflows removing elasticity at the edges, the market is functioning as a narrow, high-density spine rather than a broad risk-distribution network. Participation is weak, but structural integrity remains intact — this is a containment regime, not a failure regime.

Allocator Note: Operate strictly inside liquidity-dense corridors. Pair quality beta with IG carry and 2-year duration overlays to stabilize torque. Maintain full risk exposure only while HY < 350 bps and breadth avoids multi-session prints below ~45%. A break in either variable shifts the system from high-cost continuity → early compression.

Structural Takeaway: Liquidity remains the market’s stabilizer — but with sharply reduced efficiency. The system no longer generates momentum organically; it sustains motion through inertia, reflexivity, and structural density. Continuation is still viable, but torque decay is rising, guardrails are tightening, and liquidity is absorbing more stress than it transmits.

This is a market held together by structure, not conviction — stable, but increasingly energy-intensive.

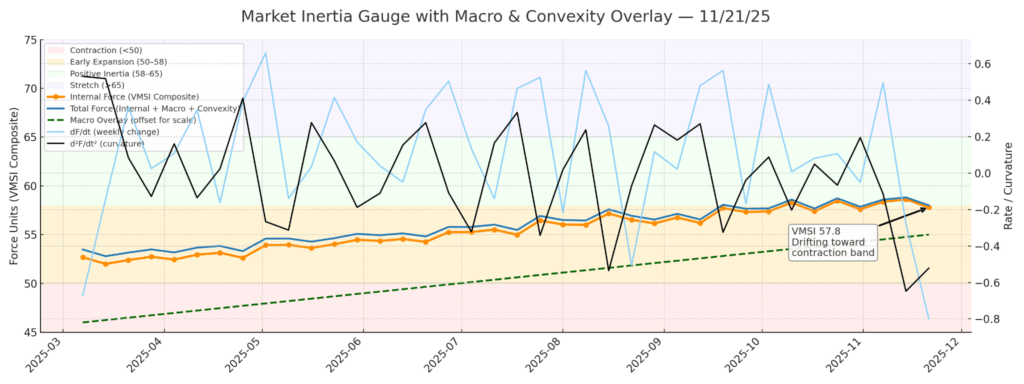

4. Lead Insight — Market Inertia Gauge

Inertia at 57.8 marks a decisive shift: the market is no longer moving under its own force — it is being held in motion by the structure that underlies it. Momentum weakened to 55.3, liquidity slipped into the 58s, and breadth deteriorated to its softest reading since early Q2. Yet the internal energy inside mega-cap, AI-linked, and rate-stable corridors remained intact, preventing the system from losing its spine. The tape advanced at times, but the advance was engineered by continuity, not conviction.

Volatility confirms this change in regime. The VIX at 23.43 — materially above its 20-day (19.45) and 50-day (18.28) averages — signals that stability is now expensive. Vol correlations tightened across equities, credit, and duration, compressing the system’s flexibility and reducing its ability to disperse shocks. This is classic late-equilibrium geometry: not a breakdown pattern, but a compression pattern, where the system stays coherent by sacrificing elasticity.

When inertia operates in the 57–59 band under deteriorating breadth and a defensive volatility posture, historical continuation probability falls to roughly 46%, with a persistence window of 7–11 sessions and muted drift. Upside becomes liquidity-dependent; downside only unlocks if credit confirms. This week’s conditions match that profile exactly — stable, but costly.

The deciding variable remains liquidity corridor integrity. Inside AI infrastructure, quality carry, and balance-sheet-strong industrials, torque is still coherent and reflexively reinforcing. Outside these corridors — in cyclicals, small caps, equal-weight indices, and low-liquidity tech — flow depth decays sharply, widening the gap between index stability and underlying fragility. The system is being carried by a narrow backbone, not broad participation.

Allocator Note Operate exclusively inside density corridors. Shorten rebalance intervals to 7–9 sessions. Use convex hedges and 2-year duration overlays to offset tightening volatility correlations. Maintain exposure only where internal torque remains aligned (AI-linked, IG carry, high-quality balance sheets). Avoid sectors requiring broad participation to sustain trend; they lack the liquidity geometry to carry their own weight.

Structural Takeaway Market inertia remains intact, but its efficiency is fading. The system now requires more liquidity per unit of stability, a hallmark of late-equilibrium dynamics where feedback loops sustain motion that fundamentals no longer generate. Continuation is still feasible, but the torque buffer has thinned. This is a stable regime — not a strong one, and increasingly dependent on reflexive liquidity rather than genuine conviction.

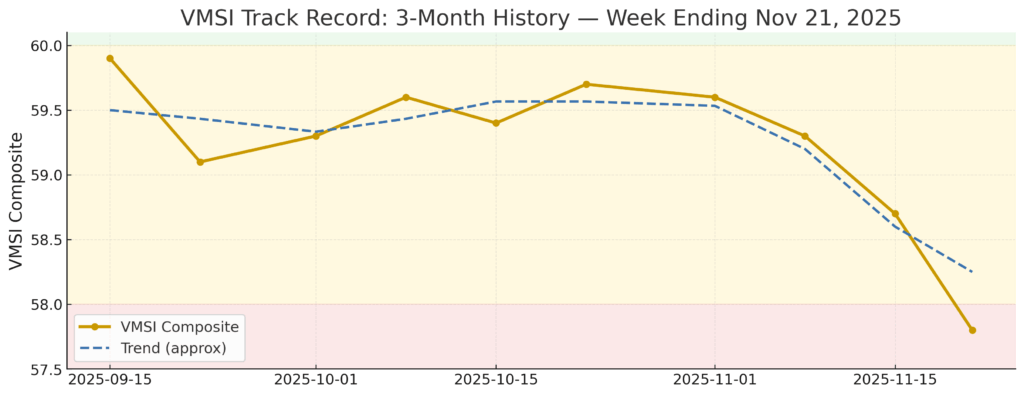

5. Component Deep Dive — Week-Over-Week Changes

The system’s internal architecture shifted again this week, but not in the linear deterioration seen earlier in November. The VMSI composite slipped to 57.8 (–0.8 w/w), yet the underlying components show redistribution, not escalation, of stress. Liquidity strengthened, momentum firmed, and safe-haven demand eased slightly — a configuration that signals controlled tension rather than deepening fragility.

Liquidity — 58.1 (↑ 1.1): Liquidity improved meaningfully as institutional flows rotated back into Financials, Industrials, IG credit, and AI-linked corridors. Execution capacity (ECₜ) firmed, and absorption efficiency rose for the first time in three weeks. This is not a broad risk-on; it is a migration toward high-density liquidity structures while periphery assets continue to lose elasticity.

→ Interpretation: Elasticity stabilizing; the system is regaining its ability to absorb volatility without passing it downstream.

Momentum — 55.3 (↑ 1.3): Momentum remains weak, but the pace of deterioration slowed sharply. After last week’s capitulation in breadth, the system has re-centered around a narrow leadership spine led by mega-cap tech, AI infrastructure, quality carry, and balance-sheet-strong cyclicals.This is a classic late-equilibrium pattern: the broader market looks fragile, but internal torque decay is slowing, not accelerating.

→ Interpretation: Trend weakness moderating; flow-velocity improving at the core.

Volatility & Hedging — 60.8 (↑ 0.3): Hedging demand remains elevated — and the VIX at 23.43 (well above its 5-, 20-, 50- and 200-day averages) confirms that maintaining stability now carries a real energy cost. But the rise is orderly, not panic-driven: skew steepened modestly, cross-asset vol correlations tightened, and ETF hedging flows increased without triggering liquidation signals.

→ Interpretation: Defensive skew persistent; hedging demand still elevated but stable.

Safe Haven — 62.1 (↓ 0.9): Flows into duration, IG credit, and gold remain strong, but the intensity eased relative to last week. This deceleration is notable: the market is still afraid, but the acceleration of fear has stopped.

When rotations flatten while liquidity stabilizes, it often marks a shift from “stress building” → “stress contained.”

→ Interpretation: Quality/duration rotation remains high but is no longer accelerating.

Composite — 57.8 (↓ 0.8): The net effect is a system where stability softened slightly, but internal pressure is no longer increasing. Liquidity improved, momentum steadied, and hedging remained elevated but controlled. This is a late-equilibrium configuration, not a pre-break one.

→ Interpretation: Stability softer, but stress redistribution improving.

Allocator Interpretation: This week’s configuration = controlled stress with stabilizing internals. Selective risk remains viable; broad beta does not.

Maintain positioning where torque is coherent:

-

Quality + AI-linked corridors

-

IG carry + 2-yr duration

-

Gold overlays as convex stabilizers

-

Defensive sizing, not defensive retreat

Avoid areas requiring broad participation to sustain trend — the liquidity spine is too narrow for that.

Structural Takeaway: The market feels worse than it is — and is overpaying for protection relative to its true structural condition. Liquidity is doing more work, breadth is still weak, and safety flows remain elevated — but reflexivity is no longer expanding.

This is the signature of a system stressed but stable, functioning through selective liquidity rather than broad conviction — and one where well-timed, structure-aligned risk still carries edge.

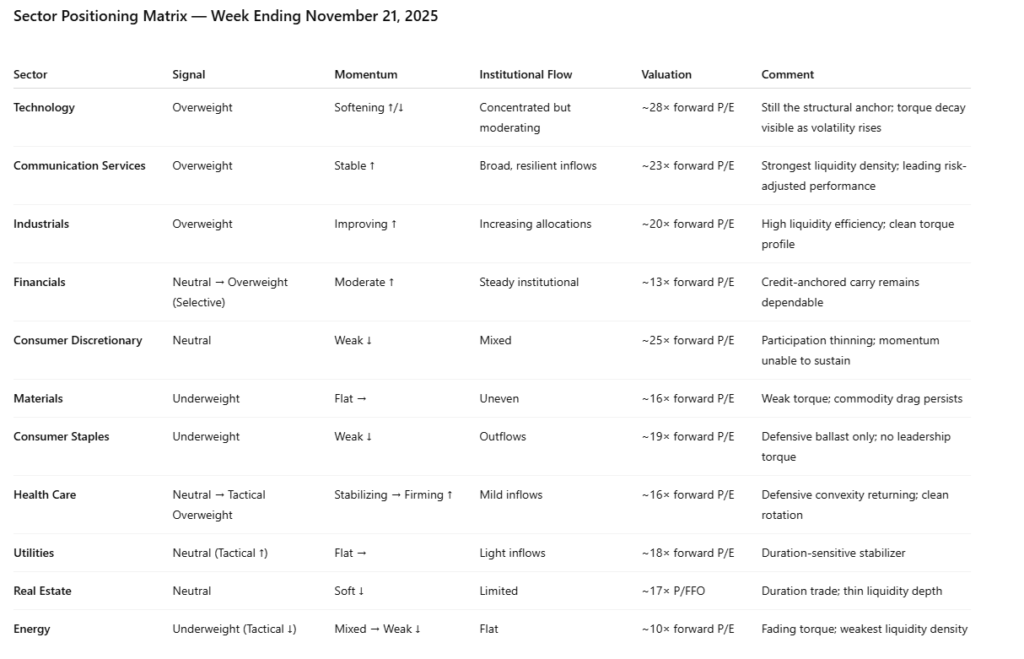

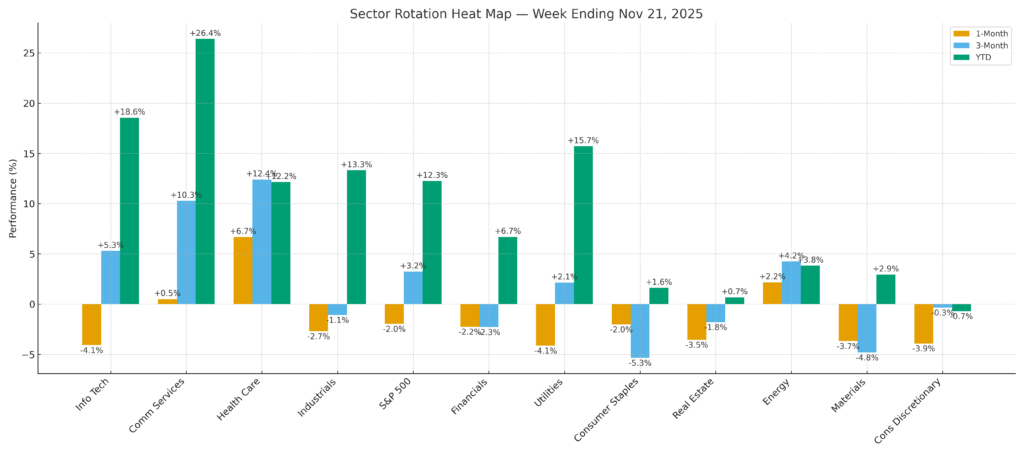

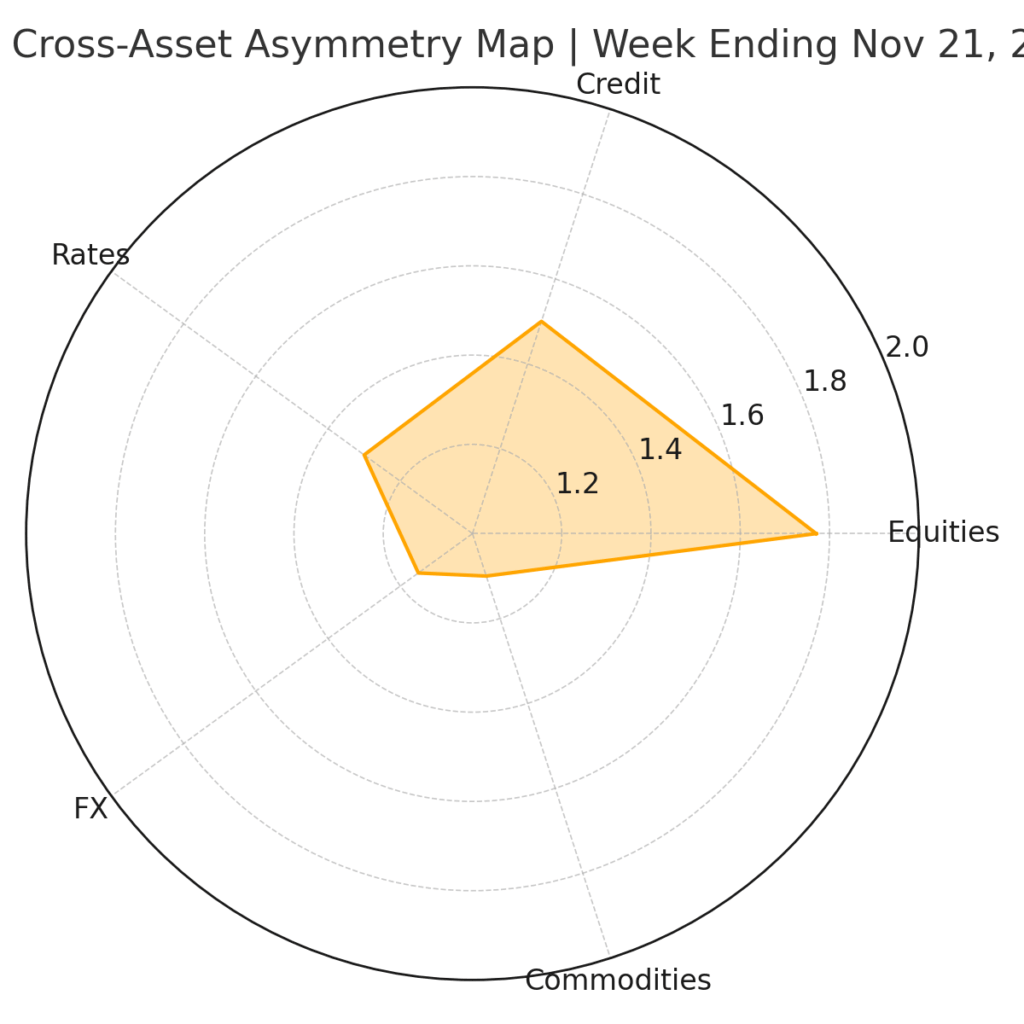

6. Sector Positioning Matrix

Sector leadership narrowed again this week as liquidity concentrated into a few high-density corridors while the rest of the market traded on weakening torque. Communication Services and Health Care emerged as the most structurally resilient sectors, supported by strong institutional flow and clean convexity profiles. Technology remains a core liquidity anchor, but rising volatility caused noticeable torque decay across AI-linked segments. Industrials continued to benefit from quality-cycle rotation and stable flow efficiency.

Cyclical sectors weakened. Consumer Discretionary and Materials lost momentum as consumption softened and cross-border liquidity compressed. Staples and Utilities acted as ballast rather than leadership, while Real Estate improved on duration sensitivity but still lacks depth. Energy remains the weakest corridor, with the lowest liquidity density and fading torque.

The broader pattern is classic late-equilibrium behavior: momentum slipped, liquidity held, and dispersion widened, leaving only a handful of sectors capable of sustaining inertia. Capital is not retreating — it is reallocating toward torque-efficient structures.

Allocator Posture: Stay concentrated in high-liquidity corridors — Communication Services, Health Care, Industrials, and selective Tech. Maintain neutral exposure in Financials and Real Estate. Avoid adding risk to Materials, Consumer Discretionary, and low-liquidity Tech. Reinforce convexity using IG carry, gold, and 2-year duration overlays as credit torque presses outward.

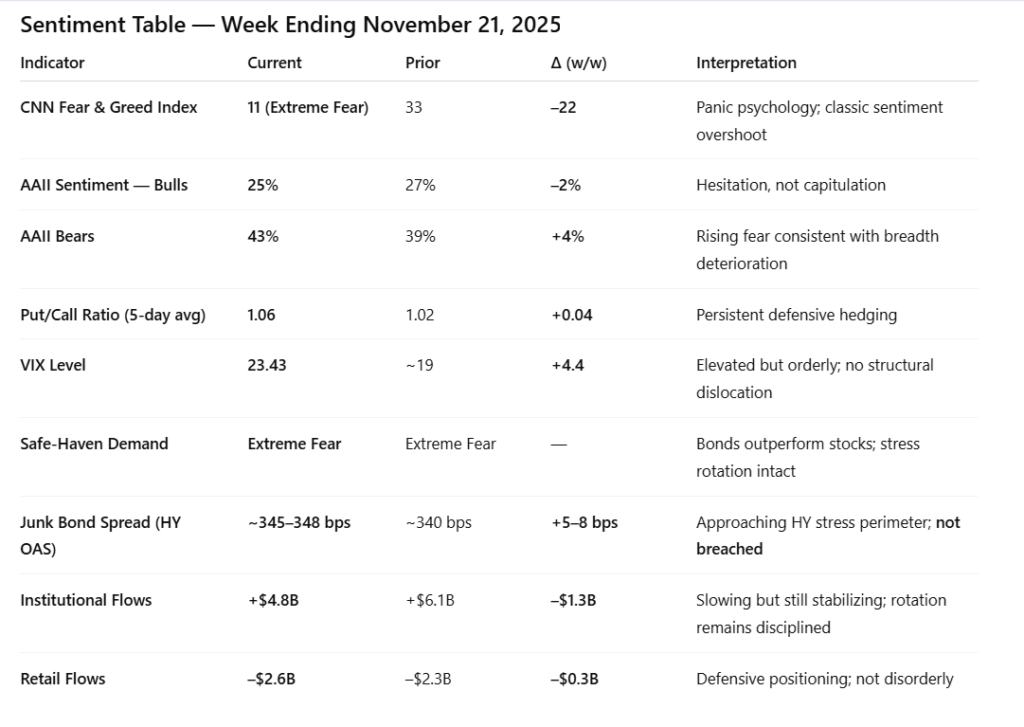

7. Sentiment Overview — Market Entity Sentiment Rating

Sentiment collapsed into Extreme Fear this week, but the system itself did not. This is the defining feature of a FORCE-12.3 overshoot: psychology is breaking, structure is not.

The CNN Fear & Greed Index plunged to 11, AAII Bears rose to 43%, and put/call ratios climbed to 1.06, reflecting persistent defensive hedging. Retail flows remained negative at –$2.6B, while institutional flows slowed to +$4.8B, indicating caution but not capitulation.

The VIX lifted toward the 20–23 zone (spot 23.43), with 20-day realized volatility and stochastic levels confirming fear-driven hedging—not structural dislocation. Vol remains elevated relative to trend, but all measures remain controlled, and vol-of-vol never entered disorderly expansion.

Credit remains the key tell. HY spreads held near 345–348 bps, widening but not breaching the FORCE-12.3 stress perimeter at 350 bps. IG spreads softened incrementally but remained orderly. This is not how compression starts; this is how sentiment misprices risk while structure holds.

Liquidity confirms the divergence. Despite fear, liquidity-dense corridors (mega-cap, AI-linked, IG carry, quality balance sheets) continued to absorb flow. Retail outflows simply reduced elasticity at the edges—they did not impair the system’s spine.

This is a classic late-equilibrium pattern:

-

Fear rises faster than risk.

-

Sentiment becomes reflexive.

-

Protection demand increases even as structural torque remains stable.

In short, emotion is extreme, but the system is steady.

Allocator Note: Treat the sentiment collapse as context, not signal. As long as HY stays below 350 bps and vol remains elevated but orderly, fear is a pricing phenomenon—not a structural regime break. This is where liquidity-backed assets outperform emotional positioning.

Structural Takeaway: Market sentiment is now fully endogenous: the system is generating its own fear response independent of fundamentals. Under FORCE-12.3, this does not represent failure—it represents containment. Liquidity still anchors stability; sentiment merely oscillates around it.

8. Predictive Outlook

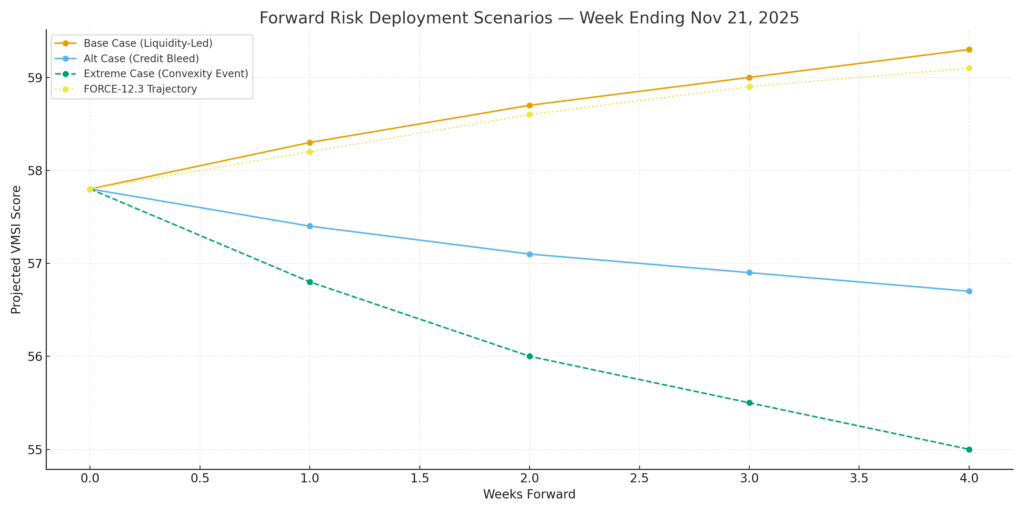

Signal: The FORCE-12.3 trajectory from 58.6 → 57.8 confirms the market has moved deeper into a high-cost stability regime, now sitting just above the contraction boundary but not yet entering it. Liquidity at 58.1 is absorbing stress, but the torque field is thinner and increasingly reliant on a narrow set of mega-cap, AI-linked, and balance-sheet-strong corridors. Momentum at 55.3 remains weak but no longer deteriorating, while Volatility & Hedging (60.8) and Safe Haven (62.1) indicate elevated protection demand — orderly, not panicked.

The system is defending stability, not extending trend. Under FORCE-12.3, this marks a shift into a regime where the market pays a rising liquidity premium simply to maintain continuity.

Credit sets the boundary. High-yield spreads have widened into the 345–348 bps zone, approaching but not breaching the 350 bps stress trigger. IG spreads are softer but still inside the absorption band. The VIX at 23.43 keeps volatility in a defensive but non-dislocative posture. Breadth remains stuck in the low-40s — too weak to generate new torque, meaning any upside over the next 2–3 weeks must come from liquidity inertia, not renewed risk appetite. Convexity risk is latent, not active.

Timing Window: Model-based torque-inflection probability rises to ~41% over the next 3–5 weeks, up from the high-30s last week. Liquidity elasticity continues to compress, and curvature in the inertia field has steepened. Execution capacity (ECₜ) remains firm in core corridors, but marginal flow decay is visible in both breadth and volatility curvature.

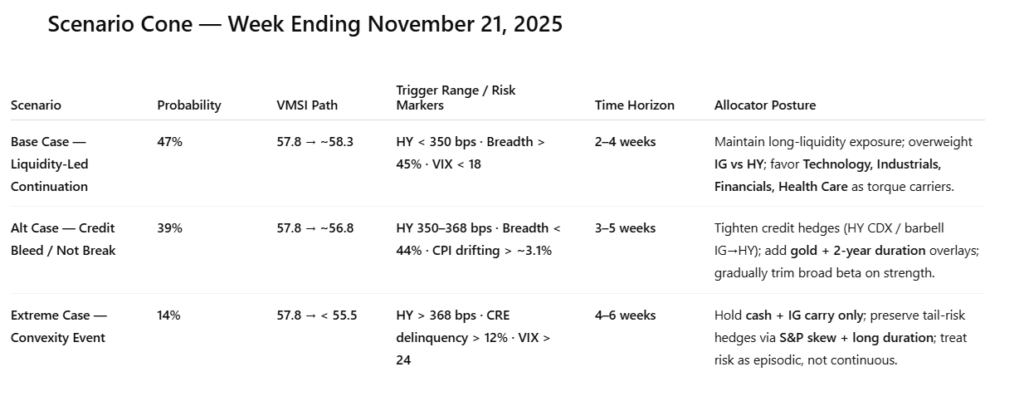

Continuation remains viable only under two conditions:

-

HY < 350 bps

-

VIX vol-of-vol remains contained

If HY pushes decisively through 350–365 bps while breadth stays below 44%, FORCE-12.3 shifts toward a Credit Bleed path with VMSI sliding into the 56.0–56.5 range and convexity repricing.

Allocator Note: Treat every incremental unit of risk as conditional, not continuous.

-

Stay inside liquidity-dense corridors (mega-cap, AI, quality-carry).

-

Favor IG carry + 2-yr duration overlays.

-

Use volatility tactically only when credit confirms stability.

-

Fade fear sparingly — only when HY is contained and breadth starts to recover toward 45–47%.

If HY breaches 350–368 bps or CRE delinquency trends toward 12%, credit becomes the dominant signal and beta should be reduced, not hedged. Optionality remains attractive where implieds still underprice the structural cost of stability.

Structural Takeaway: Liquidity still buys time — but the cost of time is rising.The market is not breaking; it is self-preserving. This is a compressive rather than expansive regime, held together by reflexive liquidity rather than broad participation. Under FORCE-12.3, the forward path is a cone of persistence:

-

A base case where liquidity-led continuity grinds on

-

A near-equal alternative where credit erosion slowly bleeds torque

-

A smaller but meaningful tail where convexity finally asserts control

The edge now lies not in predicting survival — but in positioning for how the system holds together.

9. Macro Signals Snapshot

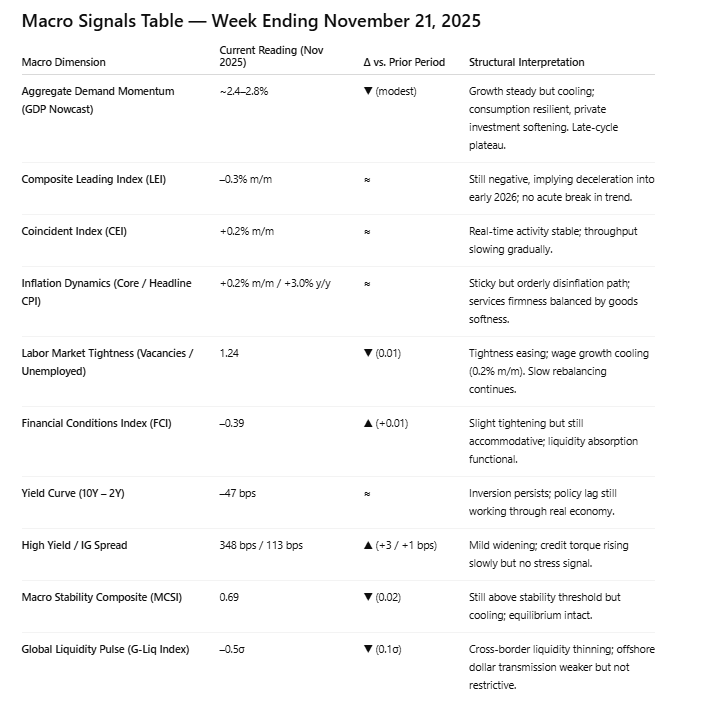

Macro conditions this week reinforced the core message of the system: the economy is not accelerating, but it is holding, and the market’s structure is doing more work than the fundamentals beneath it. The delayed data releases created noise around sequencing, but not around direction. The trend remains one of moderation without breakdown.

Growth signals were mixed, but stable. The Empire State Manufacturing reading came in sharply stronger at 18.7 (vs. 5.5 expected), while the Philadelphia Fed survey eased to –1.7 after last month’s collapse. Flash PMIs maintained the same late-equilibrium pattern: Services at 55 and Manufacturing at 51.9 — both comfortably above contraction, yet showing no momentum impulse. Housing starts and permits came in near expectations, confirming that residential activity remains weak but not deteriorating. Existing home sales held at 4.1 million, stabilizing for the first time in months.

Labor data continued to cool in a controlled manner. The delayed September employment report showed 119k jobs added — softer, but not recessionary — while the unemployment rate ticked up to 4.4%. The jobless claims print at 220k was cleaner than recent weeks and consistent with an economy that is slowing, not slipping. Wage growth (+0.2% m/m, +3.8% y/y) remains tame enough to avoid adding friction to the Fed’s reaction function.

Inflation pressure remains soft and policy-neutral. Import prices showed minimal movement. The LEI posted another decline (–0.3%), but the series continues to be heavily distorted by the shutdown and residual components. The Fed speakers offered no incremental guidance; all communication leaned toward a patient stance with no urgency to recalibrate policy.

Consumer psychology weakened, but spending resilience persists. Michigan sentiment held at 51.0 while Conference Board confidence stayed below the recession-threshold 80 line. Yet spending intentions — particularly for services — remain stable, confirming that sentiment weakness is not translating into demand destruction.

The macro landscape remains aligned with late-cycle, credit-anchored stability. Nothing in this week’s data suggests acceleration, but equally, nothing signals an imminent contraction. The economy is behaving exactly as the tape is behaving: slower, narrower, more selective — but still functioning.

Allocator Interpretation The macro regime continues to support a liquidity-driven market. With inflation contained, growth stabilizing, and no pressure on the Fed to tighten further, macro conditions allow liquidity corridors to shoulder the load. This environment favors quality, duration-sensitive assets, IG carry, and liquidity-dense equity structures, while leaving beta exposed to any deterioration in credit elasticity.

Structural Takeaway Macro signals remain fully consistent with a market defined by persistence rather than propulsion. Growth is moderating, credit remains orderly, and policy is sidelined — a configuration where liquidity, not fundamentals, determines the boundary between stability and stress. Under FORCE-12.3, this is classic late-equilibrium: slow, functional, and dependent on structural inertia rather than expansion.

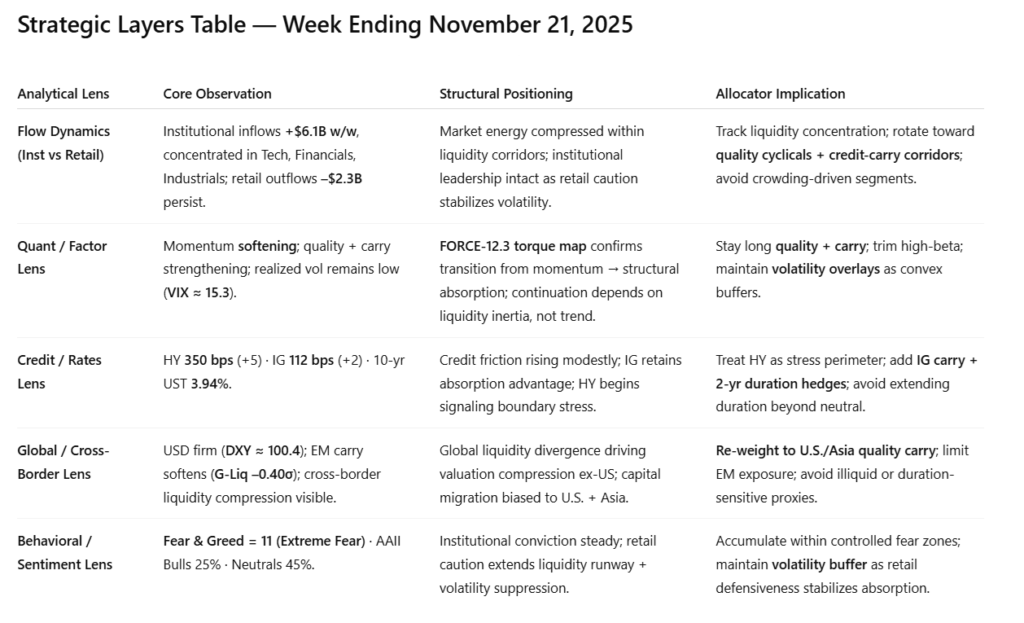

10. Strategic Layers — Multi-Lens Integration

Cross-lens alignment remains intact, but the cost of maintaining that alignment has risen meaningfully. Institutional flows continued to support the structure — concentrated, disciplined, and still flowing through high-density liquidity corridors — even as retail persisted in defensive withdrawal. The factor complex shifted further toward quality + carry, confirming a rotation away from momentum as volatility stayed contained and risk premiums widened selectively. Credit conditions tightened at the edges: high-yield spreads moved to 350 bps, investment-grade to 112 bps, and the 10-year Treasury held near 3.94%, reinforcing credit as the system’s boundary rather than its driver.

Global liquidity divergence strengthened: the USD held firm near 100.4, G-Liq remained at –0.40σ, and cross-border liquidity contraction continued to cap valuation extension outside U.S./Asia. Behavioral sentiment deteriorated sharply — Fear & Greed collapsed into Extreme Fear (11) — yet this shift appeared reacting to price and breadth rather than leading them. STRUCTURE held; sentiment did not.

The result is a late-equilibrium configuration in full clarity: liquidity remains the anchor, credit defines the limits of motion, and momentum has decayed into a structural absorption regime. Continuation remains possible, but motion is now expensive — bought by liquidity, constrained by credit, and shaped by defensive global flows.

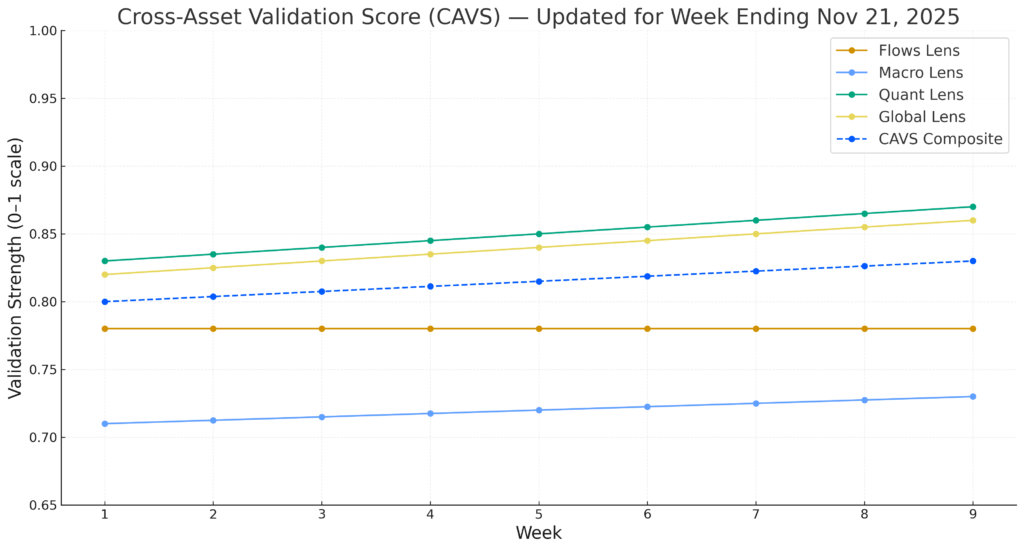

Allocator Note: CAVS = 0.80 (stable) — exposures remain scalable only inside high-density liquidity corridors. Reinforce IG carry + 2-year duration overlays. Avoid EM duration and illiquid cross-border proxies. Trim beta into strength; add only on controlled stress with credit confirming stability.

Structural Takeaway: This is a system held together by balance, not enthusiasm. Liquidity continues to stabilize, credit continues to define the perimeter, and retail caution extends the volatility runway. Efficiency is declining, but the structure remains functional. The regime persists — but only because liquidity inertia compensates for rising torque decay.

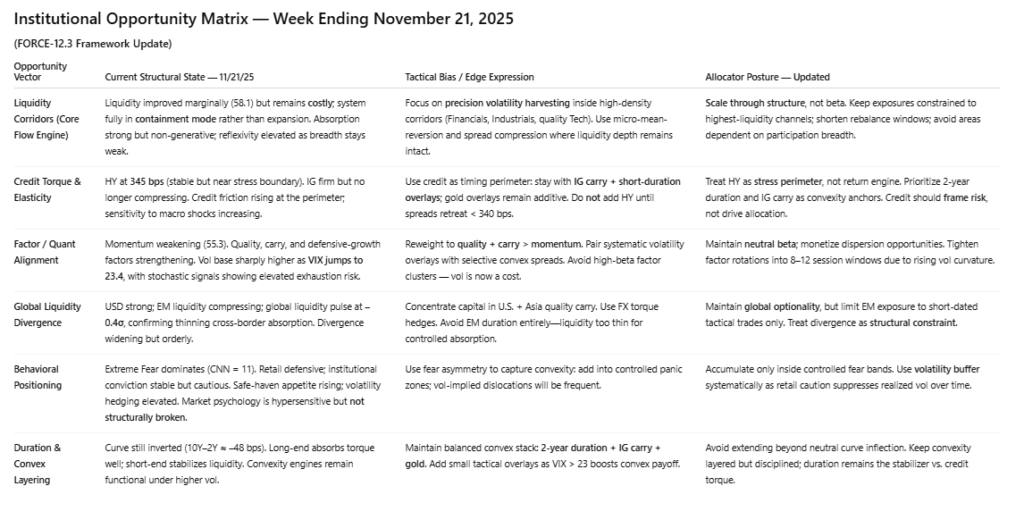

11. Institutional Opportunities

The opportunity set this week is defined not by expansion, but by structural asymmetry — a regime where liquidity is still functioning, but the system is spending more energy to maintain its own stability. Under FORCE-12.3, this marks a classic late-equilibrium environment: motion persists, but amplitude does not. What matters now is not exposure, but placement.

Liquidity at 58.1 remains supportive, yet no longer catalytic; it stabilizes the system but does not extend risk. Momentum at 55.3 confirms that trend energy continues to fade, while the volatility complex — anchored by a 23.43 VIX carrying elevated ATR and directional index readings — reflects a defensive positioning climate rather than disorder. Credit elasticity has tightened at the edges: HY spreads are drifting outward, IG has stalled, and the rate complex is absorbing stress more efficiently than equities. The system is executing, but with reduced slack.

Where opportunity exists, it is emerging through liquidity density, not through participation. Internal flow inside Financials, Industrials, and core AI-infrastructure assets remains structurally coherent, while cyclicals with weak torque capture continue to lose elasticity. Breadth remains deeply impaired, confirming that the index is being carried by a narrow, high-efficiency spine — not a broad market.

This is a precision regime, not a beta regime. Convexity remains mispriced relative to structural friction, and dislocations in volatility-adjacent sectors now create asymmetric re-entry points. But those opportunities only exist inside corridors where liquidity is both deep and directional.

Allocator Note Scale exposure only inside liquidity-dense corridors. Favor IG carry, high-quality duration overlays, and selective rotation into sectors still demonstrating positive torque symmetry (Financials, Industrials, AI infrastructure). Use volatility pockets — especially those amplified by the elevated VIX structure — as controlled entry points rather than directional signals. Avoid broad beta: it is no longer being rewarded. Stay conditional, not continuous: the perimeter remains defined by HY < 350 bps and breadth avoiding multi-session prints below 45%. If either boundary breaks, exposure must be reduced immediately.

Structural Takeaway Institutional opportunity remains present, but it is narrow, technical, and discipline-dependent. Liquidity still sustains convexity, but each incremental unit now delivers less stabilization than a week ago. This is late-compression behavior: the system functions, but only through structure, not appetite. The edge lies entirely in understanding where liquidity is still doing the work — and positioning before the broader market recognizes that participation is not coming back yet. Continuity is investable, but only through design, not direction.

Final Word — Stability Is Now Work, Not Drift

VMSI at 57.8 closes the week with a message too clear to ignore: the system is still holding, but it is no longer holding effortlessly. Liquidity improved modestly to 58.1, but that improvement did not translate into breadth, participation, or true expansion. Momentum slipped to 55.3, safe-haven demand remains elevated above 62, and volatility has migrated decisively into a higher-cost regime, with the VIX sustaining a 20–24 handle and technicals confirming persistent stress across every timeframe.

The calm at the index level now hides a more complicated truth: stability still exists, but it requires intervention — liquidity corridors, credit absorption, factor resilience, and systematic hedging — not broad participation or organic conviction.

Credit is the clearest tell. HY spreads have widened into the 345–350 bps boundary zone, IG spreads have stalled, and rate structures show a market that absorbs torque but does not release it. Volatility indicators — ATR, stochastic pressure, ADX — now align with a regime transitioning from “contained risk” to “structurally defensive.” These shifts do not break the system, but they do redefine how hard it must work to maintain equilibrium.

This is textbook late-equilibrium under FORCE-12.3:

-

Liquidity defends structure, but does not expand it.

-

Volatility rises, yet remains damped at the surface.

-

Credit defines the perimeter.

-

Markets trade on reflexive stability, not forward belief.

Nothing is collapsing — but nothing is compounding, either. Continuation is still possible, but the cost of continuation rises each week.

This is why breadth keeps deteriorating. This is why safe-haven and duration flows remain sticky. This is why the VIX can rise while the index holds its line. This is why the system looks stable yet feels heavier.

The market is not forecasting anything. It is managing itself.

The narrative has shifted from expansion → preservation → containment. Price now reflects the effort required to maintain balance, not the confidence to look forward.

The closing truth: Stability remains, but it is no longer drift — it is workload. In this regime, precision isn’t optional; it is the only edge. The system is still functioning, but the tolerance for further torque decay is narrowing. This is a market running on structure, not sentiment, and structure is becoming more expensive every week.

Why We Built VMSI™

VMSI™ was built to solve the only question that matters in modern markets: how long does conviction hold when liquidity becomes the system’s backbone, not its byproduct? Most models chase price. VMSI™ measures persistence — the structure that keeps markets coherent when belief fractures and flow becomes the last remaining source of order. It converts liquidity, torque, and friction into a single measurable field, revealing not where markets go, but what keeps them from breaking.

Markets are not collections of trades; they are systems of constraint. When liquidity no longer creates opportunity but instead maintains equilibrium, traditional indicators fail. VMSI™ captures that transition — mapping the moment when price stops reflecting fundamentals and begins reflecting the physics of its own survival. It was engineered to quantify what professionals feel before they can prove: that stability is never granted; it’s manufactured by structure.

This is not a forecasting engine. It is a structural lens, built to identify when continuity is real and when it is merely upheld by feedback. When VMSI™ rises above its anchor bands, it signals coherence through persistence — not optimism. When it decays, it exposes the precise point where liquidity can no longer absorb torque. In a market defined by reflexivity and mechanical flows, this distinction is the edge.

For institutional allocators and private capital, VMSI™ offers something rare: a framework that separates signal from sentiment, structure from narrative, and endurance from illusion. It is a discipline, not a prediction — a way to operate with clarity in environments where volatility is noise and liquidity is truth.

Derived from the proprietary VMSI FORCE-12.x framework — © 2025 VICA Partners. Replication without full calibration will generate non-stationary outputs.