“Empowering Financial Success” Vica Partners Financial Group

MARKETS TODAY – September 7th, 2023 (Vica Partners)

Global Markets Snapshot

- In Asian markets, we saw a decline today. Hong Kong’s Hang Seng index dropped by 1.34%, China’s Shanghai Composite was down by 1.13%, and Japan’s Nikkei 225 saw a 0.75% decrease.

- In the US, S&P futures opened 0.69% below fair value for today’s trading.

- European markets had a mixed performance. London’s FTSE 100 gained 0.21%, France’s CAC 40 rose by a slight 0.03%, while Germany’s DAX lost 0.14%.

US Markets Today

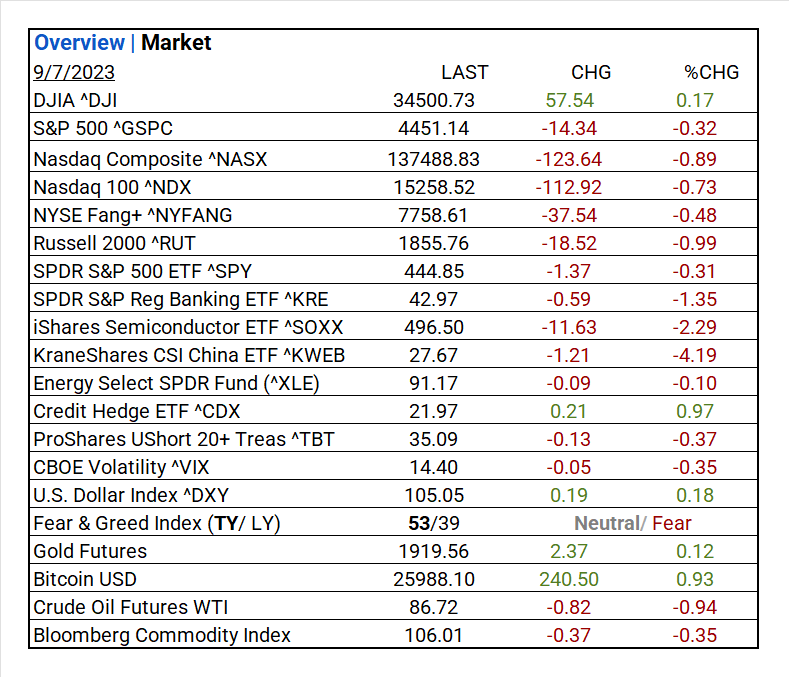

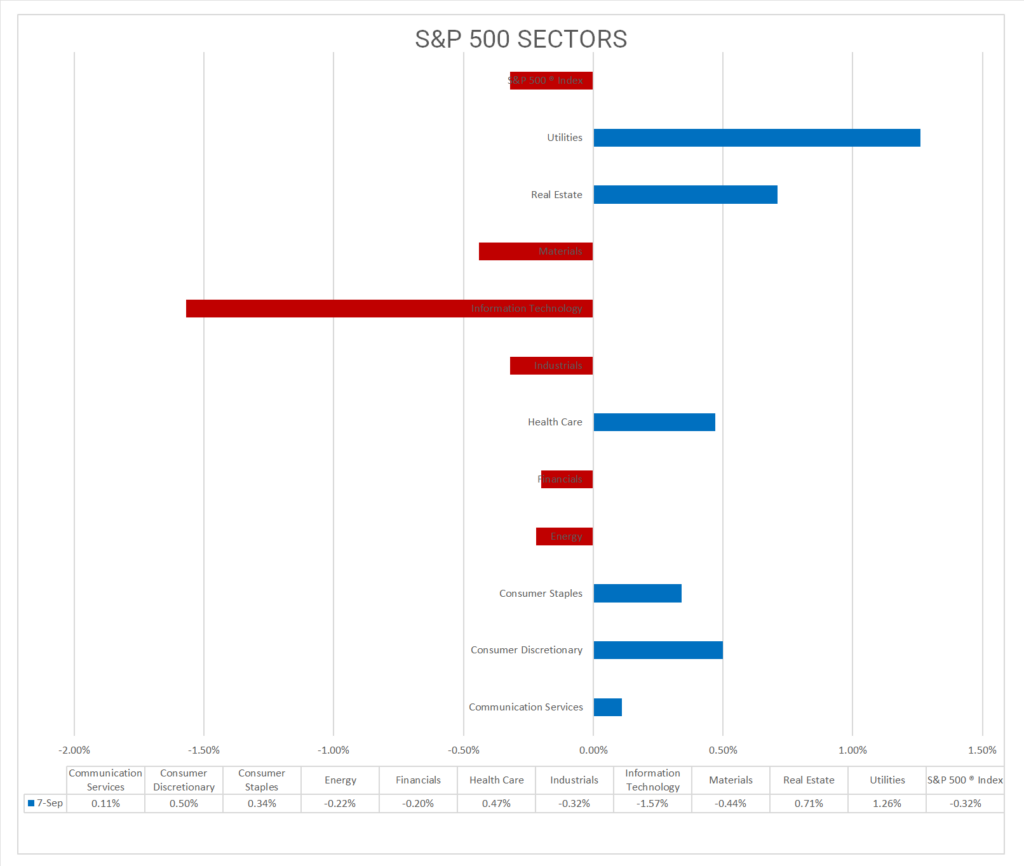

- US stock markets finished mixed, the DOW up 0.17%, the S&P 500 saw a 0.32% decline the NASDAQ fell by 0.89%. Among the 11 S&P 500 sectors, 5 experienced declines. Utilities performed the best, with a gain of +1.26%, while Information Technology took a significant hit, plummeting by -1.57%. Notable industries that stood out for the day included Broadline Retail (+1.71%), Industrial REITs (+1.59%) and Gas Utilities (+1.57%). Additionally, the Credit Hedge ETF (^CDX ETF) posted gains of 0.97%.

US Economic Highlights

- In economic news, there was a notable decrease in both initial claims and continuing claims. Initial claims dropped to 216,000 from 229,000, and continuing claims decreased to 1.68 million from 1.73 million. FDIC released its Q2 Quarterly Banking Profile, there was no change to the number of banks on the problem list.

Key Takeaways

- Inflation Concerns Renewed by Labor Data: The day brought concerns about inflation back into focus as both initial claims and continuing claims for unemployment benefits saw a significant drop.

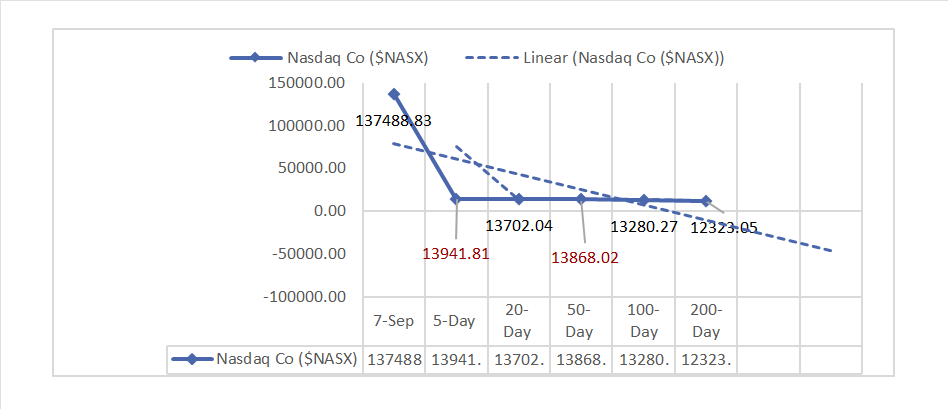

- Tech Market Faces Challenges: The Nasdaq Composite led the decline among major indices, primarily due to Apple (AAPL) facing setbacks. This was triggered by news of China restricting government iPhone usage.

- Top Performers: Standout performers for the day were Broadline Retail (+1.71%), Industrial REITs (+1.59%), Gas Utilities (+1.57%), Water Utilities (+1.46%), Multi-Utilities (+1.39%).

- Credit Hedge ETF Gains: The Credit Hedge ETF (^CDX) saw a rise of 0.97%.

- Strength of the US Dollar: The US Dollar Index (^DXY) once again demonstrated its strength.

- Bitcoin Bounces: Up today 0.93% with $240.50 price move.

- Strong Earnings from Smartsheet: Smartsheet (SMAR), reported impressive earnings, surpassing expectations.

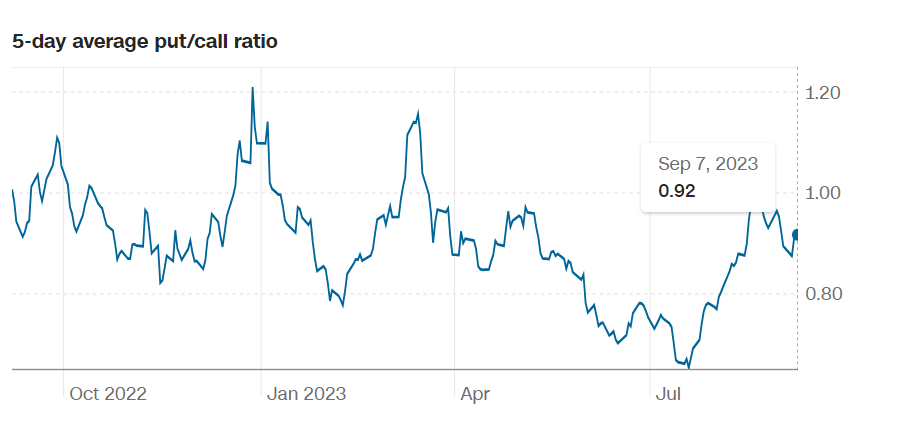

Pro Tip: When the put-to-call ratio is on the rise, it typically indicates that investors are becoming increasingly apprehensive. A ratio exceeding 1 is commonly interpreted as a bearish signal.

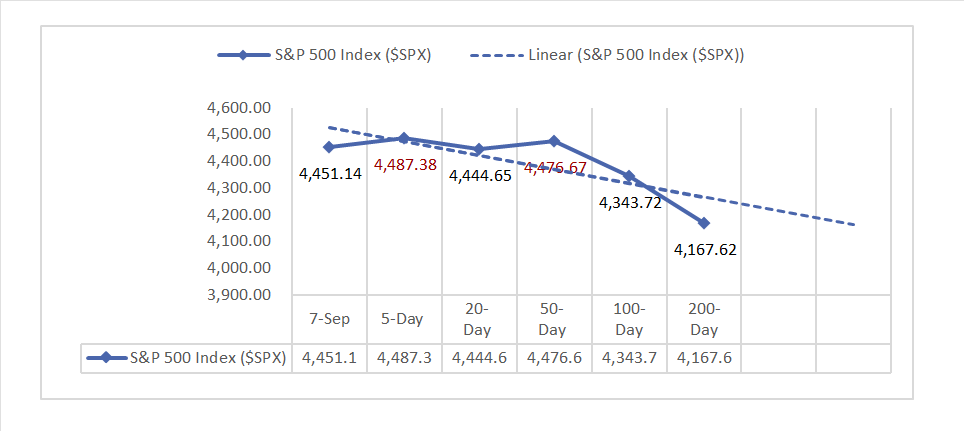

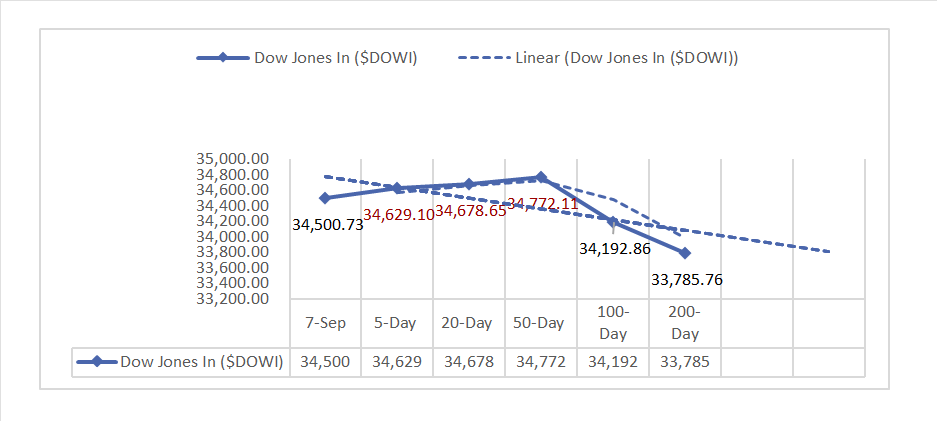

Indices, Sectors, Factors, and Treasuries

S&P Sectors

- S&P 500 Sector Update (as of September 07, 2023):

- Out of the 11 S&P 500 sectors, 6 made gains.

- Utilities outperformed all, with a solid increase of +1.26%.

- However, Information Technology experienced a significant decline, dropping by -1.57%.

- Top-Performing Industries for the Day

Some noteworthy industries for the day included:

- Broadline Retail (+1.71%)

- Industrial REITs (+1.59%)

- Gas Utilities (+1.57%)

- Water Utilities (+1.46%)

- Multi-Utilities (+1.39%)

- Health Care Providers & Services (+1.37%).

- Performance Over the Past Month (as of September 06, 2023):

- The Energy sector took the lead with an impressive gain of +4.88%.

- Information Technology followed closely with a +2.15% increase.

- Communication Services also posted a notable gain of +1.43%.

- Year-to-Date (YTD) Leaders in the S&P 500 (as of September 06, 2023):

In terms of year-to-date performance, the top three sectors in the S&P 500 are:

- Communication Services (+42.65%)

- Information Technology (+42.59%)

- Consumer Discretionary (+31.62%).

- Overall, the S&P 500 showed a substantial gain of 16.30%.

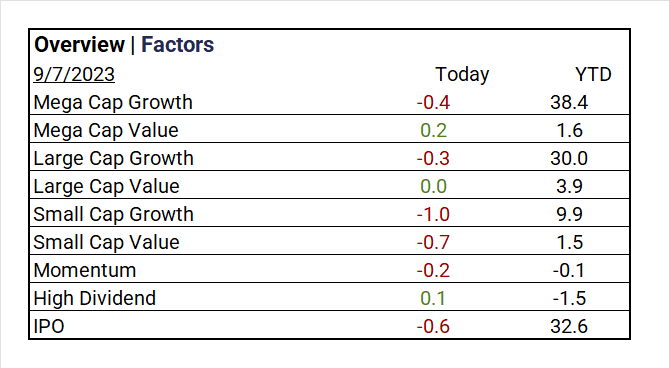

Factors

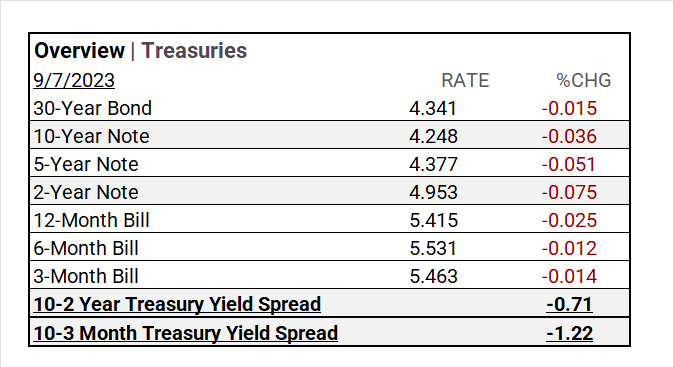

US Treasuries

Earnings

- In Q1 ’23, 79% of companies beat analyst estimates by an average of 6.5%.

- The Q2 Forecast predicted a decline of <7.2%> in S&P 500 EPS, with Fiscal year 2023 EPS remaining flat YoY.

- Q2 Seasonal Actuals are yet to be reported.

Notable Earnings Today

- +Beat: DocuSign (DOCU), Science Applications (SAIC), BRP Inc (DOOO), Smartsheet (SMAR), Braze (BRZE) Korn Ferry (KFY), G-III Apparel (GIII)

- -Miss: Sekisui House ADR (SKHSY), Toro (TTC), RH (RH), ABM Industries (ABM), John Wiley&Sons (WLY)

Economic Data

US

- Initial jobless claims (Sept. 2): 216,000 (Previous 229,000, Forecast 230,000)

- U.S. productivity (revision)(Q2): 3.5% (Previous 3.7%, Forecast 3.4%)

- Unit-labor costs (revision) (Q2): 2.2% (Previous 1.6%, Forecast 1.9%)

“Navigating September 2023: Vica Partners Insights”

- Our aim with this report is to provide you with a comprehensive overview of the prevailing trends that are shaping financial markets.

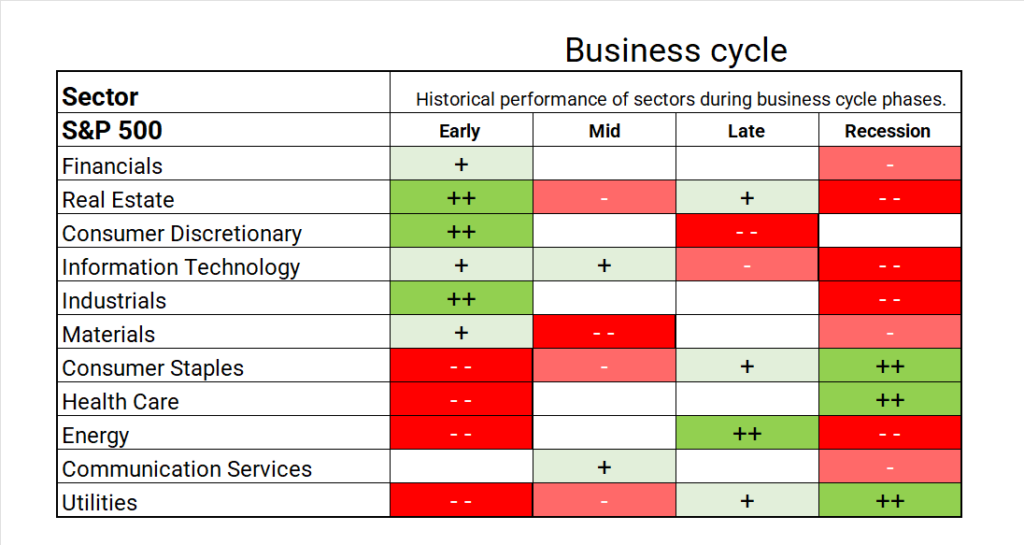

Key Trends

- Growth stocks tend to perform well during economic optimism.

- ^NYFANG new defensive’s Index as “bigger allows for more capital to scale”

- AI and Semiconductor Equipment will continue to outperform.

- Market had a Factor regression from Growth to Value stocks in the past 45 days.

- Energy is August Sector leader and look for further ’23 opportunity here.

- Health Care +Health Care REITs and Materials undervalued.

- Current economic signals are mixed with deflation concerns.

- August/September historically have lower ROI.

“Vica Partners: Navigating the Economic Landscape – 2023 Economic Forecast

- As of September 2023, the Federal Reserve no longer predicts a recession. However, Vica Partners disagrees and forecasts a potential recession starting as early as Q4 ’23 and extending into ’24. This projection is based on factors including Fed tightening, rising oil prices, overvalued stock markets, and a strong dollar. Vica Partners believes that market bottoms typically occur amid negative news and deflationary signals. Rising interest rates and their impact on the real estate market, coupled with historical highs in consumer debt, are significant concerns. Vica Partners also notes the shift from Growth to Value stocks and the moderation of the Information Technology sector correction occurred.

Key Points

- The Federal Reserve’s power to control inflation is limited, and traditional economic principles may not be effective in today’s highly automated global economy.

- A 2% inflation target may not be realistic today, and a base rate exceeding 3% could fund wage increases, energy transition, operational efficiency improvements, and protection against deflation.

News

Company News/ Other

- Apple Faces New Challenge in China as Huawei Releases High-Speed Phone – WSJ

- TikTok’s New Amazon Copycat Is Full of Cheap Chinese Goods – Bloomberg

- Whose Rail Line Is It Anyway? Freight Carriers Could Be Forced to Share Tracks With Competitors – WSJ

Energy/ Materials

- Saudi Move Boosting Oil Prices Raises Political Risk for Biden – Bloomberg

- China Is the Oil and Gas Crowd’s Biggest Unknown – Bloomberg

- Texas Grid Faces Another Test With Power Experts Assessing Near Mis – Bloomberg

Real Estate

- Cities Need People, People Need Homes. Both Must Wait – Bloomberg

- Real-Estate Doom Loop Threatens America’s Banks – WSJ

Central Banks/Inflation/Labor Market

- US Initial Jobless Claims Slide to Lowest Level Since February – Bloomberg

- Why Higher Unemployment Is Good News Now – WSJ

Asia/ China

- US raises alarm as Chinese platform corners market on global shipping logistics – SCMP