Markets are transitioning from risk recalibration into accelerating internal deterioration, not structural breakdown. Equity momentum weakened further across all major indices, volatility expanded materially, and credit spreads widened modestly while remaining functional. Treasury markets remain orderly, though rate volatility has accelerated and is now exerting clear influence across assets.

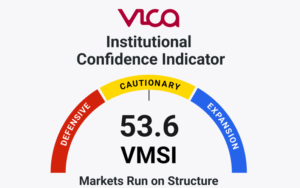

The VICA Institutional Market Sentiment Index (VMSI) declined to 52.4, signaling a shift from stable institutional participation toward broader and more active de-risking beneath the surface.

VMSI is a proprietary framework that synthesizes cross-asset signals including volatility regimes, credit spreads, liquidity flows, and institutional positioning to identify shifts in market structure.

The central signal this week is the alignment between weakening momentum and expanding volatility, confirming active exposure reduction rather than passive stabilization.

Structural Signal: Institutional positioning is transitioning from defensive stability toward accelerating de-risking, with momentum deterioration leading, volatility expanding, and credit conditions still orderly. This configuration historically precedes downside-biased consolidation — not immediate recovery.

VMSI Regime Signal: Accelerating deterioration following volatility expansion.

Capital Positioning Signal

Current signals suggest institutions are reducing marginal equity exposure while maintaining core allocations, with volatility hedging elevated and credit markets continuing to signal systemic stability.

The shift is not liquidation — it is de-grossing. Positioning reflects risk compression and duration reduction, not capital exit.

CIO Decision Snapshot

Market Regime: Transition from risk recalibration to accelerating de-risking with stable but tightening liquidity conditions.

Near-Term Catalyst: Federal Reserve policy guidance and Treasury yield behavior, particularly whether rate volatility stabilizes or continues to expand.

Market Regime Snapshot

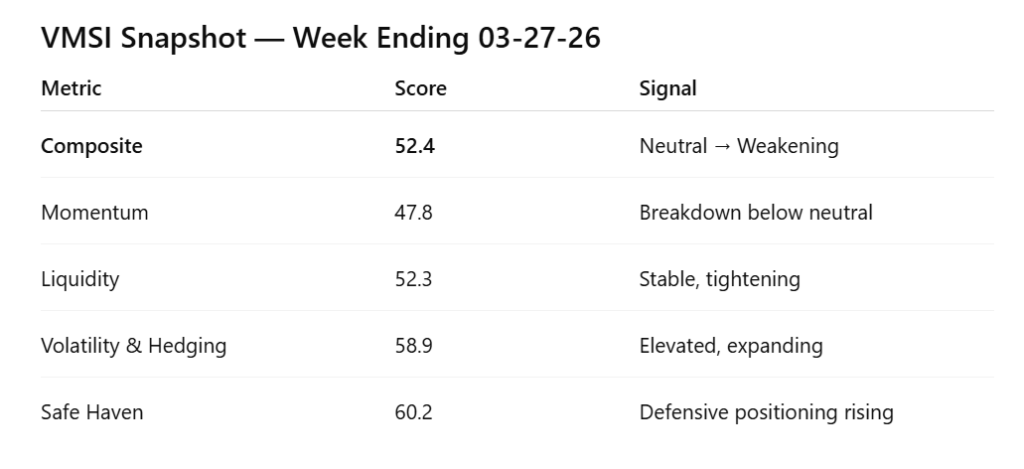

VMSI Sentiment: 52.4 — Neutral / Defensive Drift

VMSI has remained above the Neutral threshold for 54 consecutive weeks, but momentum remaining below 50 now confirms a critical institutional inflection point.

Equity Structure: Broad short-term breakdown with weakening intermediate structure. The S&P 500 is now trading below its 5-, 20-, and 50-day averages while approaching its 200-day support near 6,635.

Risk Transmission: Hedging is no longer isolated to equities — it is spreading through rates and duration, signaling deeper cross-asset pressure.

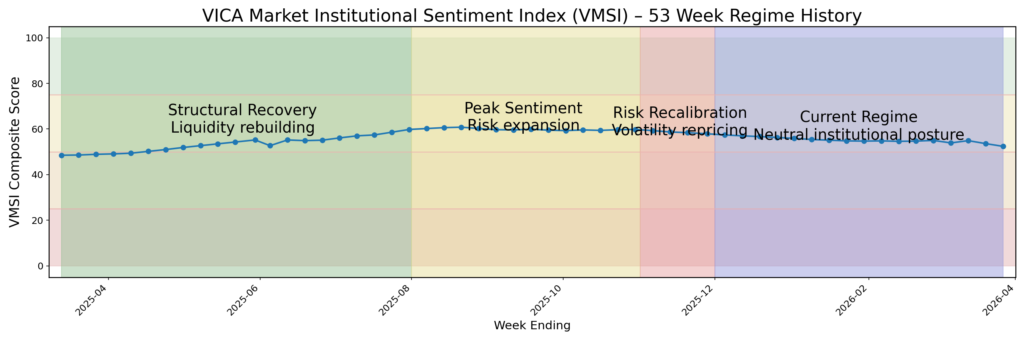

VMSI 53 Week Regime History

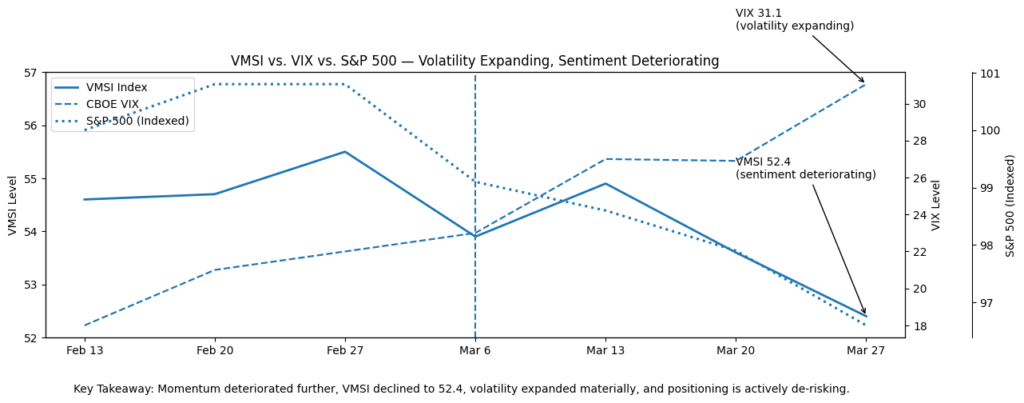

VMSI vs. VIX vs. S&P 500

VMSI Historical

The VMSI tracks institutional risk posture across volatility, credit, liquidity, and macro signals. Over the past year the index has moved through four identifiable phases: structural recovery, peak sentiment expansion, volatility repricing, and the current transition into a neutral-to-defensive regime.

VMSI vs. VIX vs. S&P 500

The relationship between VMSI, volatility, and equity performance now shows sentiment weakening alongside expanding volatility, confirming active exposure reduction rather than stabilization.

Market Structure

Major equity indices weakened further across short-term and intermediate trend windows.

The S&P 500 closed at 6,368, trading below its 5-, 20-, and 50-day averages and below its 200-day trend near 6,635. Momentum has accelerated to the downside, with RSI in the high-20s to low-30s depending on lookback.

The Nasdaq Composite closed at 20,948, trading more than 10% below its 50-day average and more than 11% below its 100-day average, reflecting continued pressure on long-duration assets.

The Dow Jones Industrial Average closed at 45,166, with RSI near the high-20s to low-30s, confirming broad cyclical participation in the drawdown.

Small-cap equities remain highly sensitive to tightening liquidity. The Russell 2000 proxy (IWM) closed at 243.10, below its 20- and 50-day averages, though still holding modestly above its 200-day level.

When both short- and intermediate-term structures break while credit remains intact, markets typically enter downside-biased consolidation — not systemic failure.

Volatility Regime

Volatility has moved from elevated to expanding.

The VIX closed at 31.05, remaining significantly above its 20-day and 50-day averages.

The broader volatility complex shows expansion beyond equities:

VVIX ~133 → sustained convexity demand

VXN ~33.5 → continued Nasdaq hedging

SKEW ~144 → stable tail-risk demand without panic

MOVE ~115 → critical regime escalation

System Stability Check: Rate volatility is now the dominant transmission channel, increasing the probability of continued multiple compression.

Rates and Duration

Treasury markets remain structurally stable but are undergoing accelerated repricing driven by volatility, not liquidity stress.

SHY: 82.39 → stable front-end

IEF: 94.60 → below short-term averages

TLT: 85.64 → below 20-, 50-, and 100-day trends

Convex duration exposures (EDV, ZROZ) continue to weaken.

Conclusion: Rate volatility — not direction — is now driving asset repricing across equities.

Credit Conditions

Credit markets weakened modestly but remain functional.

HYG: 78.72 → below short-term averages, near structural support

LQD: 107.62 → weakening in line with rates

EMB: continued decline → tightening global liquidity

Momentum signals indicate controlled spread widening, not disorderly repricing.

Key Insight: Credit remains the system anchor. If credit breaks, the regime changes immediately.

Factor Rotation

Factor dispersion continues across equities.

VTV (Value): 193.35 → relatively resilient

VUG (Growth): 422.37 → materially below 50- and 100-day averages

Rotation is ongoing — but no longer stabilizing markets.

Global Risk Signals

Global markets weakened in coordination.

EEM: 55.20 → significant drawdown vs 20-day

EWJ: sharp decline

FXI: structurally weak

DXY: 100.17 → firm and rising

GLD: 414.70 → rebound from prior liquidation, but still well below its 20-day average

Signal: Tightening global conditions without full capitulation.

Economic Backdrop

Economic data reflects stable inflation with rising forward uncertainty.

PPI and import prices remain elevated → inflation persistence

Jobless claims: ~210K → labor stability

Forward indicators (consumer confidence, retail sales, ISM, payrolls, and Fed communication) now matter more for rate volatility than realized growth alone.

Macro regime: Late-cycle stability with rising volatility risk.

VICA Institutional Market Sentiment Index (VMSI)

Institutional sentiment weakened further as internal conditions deteriorated and volatility expanded across both equities and rates.

VMSI Metrics Week Ending 3-27-26

Bottom Line

Markets are transitioning from risk repricing into accelerating de-risking, not systemic instability.

Momentum deterioration, expanding volatility, and rising rate instability are driving risk compression and multiple adjustment, while credit remains stable.

This environment favors downside-biased consolidation — not collapse.

Key Asymmetry: If credit spreads widen materially, markets shift from orderly de-risking → accelerated downside repricing.

The next directional move will be driven by Fed signaling and rate volatility stabilization.

About the VICA Institutional Market Sentiment Index (VMSI)

The VICA Institutional Market Sentiment Index (VMSI) is a proprietary framework designed to track shifts in institutional risk behavior across global markets.

The index integrates cross-asset signals including momentum, liquidity flows, volatility hedging demand, credit conditions, and safe-haven allocation trends.

VMSI scores are generated through a systematic model combining volatility regimes, credit spreads, liquidity flows, macroeconomic signals, and institutional positioning indicators to identify shifts in market structure.

Index Scale

0–25: Systemic Risk / Defensive Positioning

26–49: Elevated Risk / Cautious Allocation

50–74: Neutral / Balanced Institutional Exposure

75–100: Expansion / High Institutional Risk Appetite

Important Notice

This report and the proprietary VICA Institutional Market Sentiment Index (VMSI) are confidential works protected by intellectual property laws. Unauthorized reproduction or redistribution is prohibited.

This material is for informational purposes only and does not constitute investment advice.

VICA Research

The VICA Research platform and VMSI dashboard will relaunch in April 2026, introducing expanded institutional data tools and cross-asset analytics.

Capital does not follow headlines. It follows structure.

Week Ahead Executive Takeaway Markets are transitioning from risk recalibration into early-stage internal deterioration, not structural breakdown. Equity momentum weakened...

Week Ahead Executive Takeaway Markets are undergoing risk recalibration rather than structural deterioration. Equity momentum weakened across major indices while...