Institutions Are Buying Again. Commitment Has Not Followed.

April 11, 2026

Matthew Krumholz

VMSI REPORT 04-10-26

VMSI Snapshot

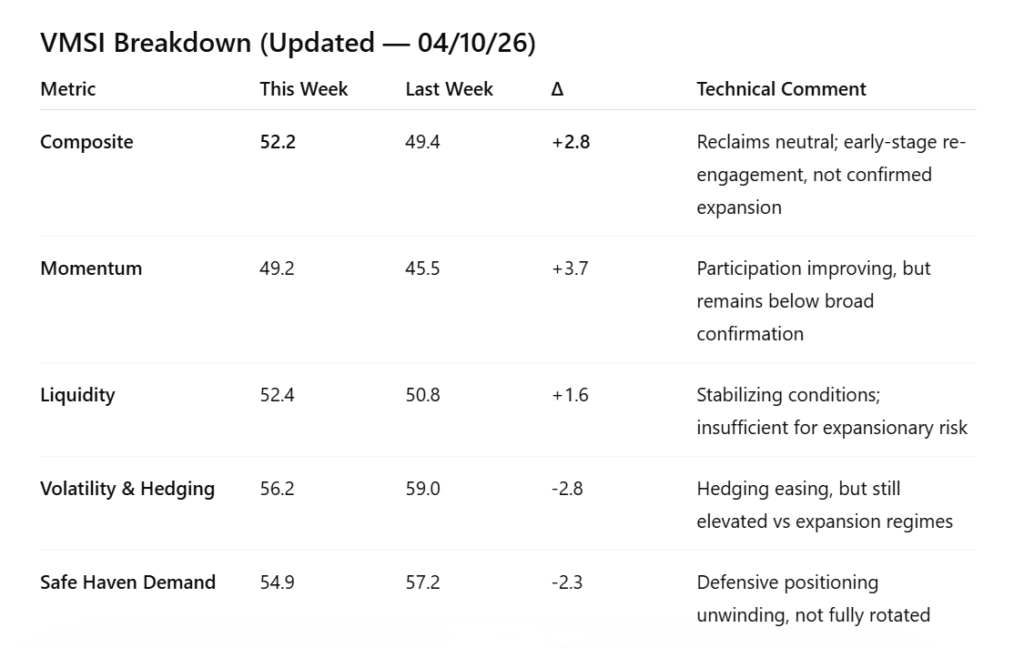

The VMSI increased to 52.2 (+2.8 WoW), driven by improving credit conditions and renewed equity inflows.

Momentum: 49.2

Liquidity: 52.4

Volatility & Hedging: 56.2

Safe Haven Demand: 54.9

The index has moved back above neutral, but remains below expansionary levels.

Executive Summary

High yield spreads tightening to 2.90% (−23 bps) and +$17.9B equity inflows confirm re-engagement, but +$8.9B bond flows and CPCI at 0.98 show positioning has not rotated.

HY OAS: 2.90% (−23 bps WoW)

Equity ETF flows: +$17.9B

Bond ETF flows: +$8.9B

CPCI: 0.98 | CPCE: 0.68

The data reflects a market reopening to risk, but still structurally cautious.

Capital is moving. Conviction is not.

VMSI

VMSI Index 4-10-26

Market Structure Analysis

Credit Conditions

High yield OAS at 2.90% (−23 bps) marks a material easing in financial stress, but remains above expansion thresholds.

High Yield OAS: 2.90% (−23 bps WoW)

Investment Grade OAS: 0.83% (−4 bps WoW)

This improvement stabilizes financing conditions, but does not yet confirm broad risk acceptance.

Credit is stabilizing, not confirming expansion.

Flow Data (Confirmation Layer)

+$17.9B equity inflows alongside +$8.9B bond inflows indicate participation without reallocation.

Equity ETF flows: +$17.9B

Bond ETF flows: +$8.9B

Institutions are adding exposure, but not shifting portfolios.

Buying returned. Rotation did not.

Equity Factor Rotation

Value leadership (+5.4% YTD VTV) and growth weakness (−5.5% YTD VUG) confirm defensive allocation bias.

VTV: +5.4% YTD, above trend

VUG: −5.5% YTD, below 50D / 100D

Leadership remains anchored in durability, not beta.

Exposure increased. Risk appetite did not.

Positioning & Hedging

CPCI at 0.98 and CPCE at 0.68 show hedging has declined, but remains above expansionary levels.

CPCE: 0.68

CPCI: 0.98

Institutions are reducing protection incrementally, not removing it.

Protection is reduced, not removed.

What Changed This Week

HY spreads tightening (−23 bps) and +$17.9B equity flows mark improving conditions, but CPI at 0.9% and persistent bond demand constrain transition.

HY OAS: −23 bps → 2.90%

Equity flows: +$17.9B

Small caps: ~+4% weekly

CPI: 0.9% MoM

Bond flows: +$8.9B

The pace of improvement accelerated, but macro constraints remain binding.

Signals are improving, but not aligned across asset classes.

The system is stabilizing, not synchronizing.

What Most Are Missing

Credit at 2.90%, balanced flows (+$17.9B / +$8.9B), and CPCI at 0.98 show stabilization—not expansion.

Credit improved, but not expansionary

Flows returned, but remain balanced

Hedging declined, but persists

The improvement is real, but incomplete.

Conditions improved. Belief did not.

Bottom Line

HY OAS (2.90%), flows (+$17.9B equities / +$8.9B bonds), and CPCI (0.98) confirm re-engagement without full commitment.

HY OAS: 2.90% (−23 bps)

Equity flows: +$17.9B

Bond flows: +$8.9B

CPCI: 0.98

Markets are stabilizing, but not transitioning.

Institutions are buying again. Commitment has not followed.

Access the Full Institutional Report

The full VMSI report — including factor-level breakdowns, regime probabilities, and forward positioning signals used by institutional allocators — will be available with the VICA Partners relaunch this week.

The relaunch introduces an institutional platform focused on real-time sentiment tracking, capital flow analysis, and cross-asset structure for allocation decisions.

VICA Partners Research

About the VICA Institutional Market Sentiment Index (VMSI)

The VMSI is VICA Research’s proprietary sentiment gauge designed to track shifts in institutional risk behavior, capital flow posture, and macro-driven volatility signals.

Each weekly score reflects a multi-factor model that incorporates market structure, liquidity dynamics, defensive rotation, and volatility hedging.

Index Scale

0–25: Critical Risk Zone

26–49: Defensive

50–74: Cautionary Optimism

75–100: Expansion / High Confidence

Important Notice

This report and the proprietary VICA Market Sentiment Index (VMSI) are confidential and protected. Unauthorized use is prohibited.

VICA Research

Capital does not follow headlines. It follows structure.