Markets have stabilized in price, but the system beneath them remains constrained. Credit has improved tactically without normalizing structurally, while liquidity has increased without transmitting into risk.

Markets are stabilizing in price, but not in structure.

Executive Briefing

Markets are stabilizing within a still-restrictive financial system.

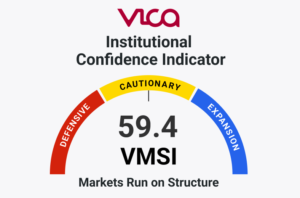

The VICA Institutional Market Sentiment Index (VMSI) declined to 49.4 (−3.0 WoW), moving below neutral and signaling a shift toward defensive positioning.

Credit tightened on the week, with high yield spreads compressing −26 bps, yet remain +8 bps above the one-month baseline (3.08%). Liquidity increased by over $46B, but failed to transmit into tighter financial conditions.

Capital is holding exposure — not committing to risk.

VMSI Index 4-3-26

Interpretation

The system is defined by a failure of transmission.

High yield spreads tightened to 3.16% (−26 bps WoW), but remain +8 bps above the one-month baseline, while investment grade spreads at 0.87% remain +5 bps above baseline. This establishes a clear acceleration profile: short-term compression within a still-tight structural regime.

Liquidity increased materially, with the Fed balance sheet rising +$18.2B and reserves +$28.4B, yet spreads did not compress below baseline. In a functioning expansion phase, liquidity would lower the cost of capital. It is not doing so.

At the same time, the dollar remains firm near 100, maintaining global tightening conditions.

Liquidity is supporting the system — not advancing it.

Key Signal

Neutral Market. Defensive Capital.

Credit remains above baseline, liquidity is non-transmissive, and volatility remains elevated. These conditions allow markets to stabilize, but prevent capital from expanding into risk.

This is a market that can hold — but cannot yet move forward.

What Changed

The rate of change shifted, but the structure did not.

Credit spreads compressed week-over-week (HY −26 bps), and liquidity increased by more than $46B, slowing the pace of deterioration. However, spreads remain wider than one month ago (HY +8 bps, IG +5 bps), confirming that financial conditions have not eased.

The pace of deterioration has slowed, but the system has not improved.

Cross-Asset Interpretation

There is no cross-asset confirmation of expansion.

Equities are advancing, but participation remains incomplete, with only 47% of stocks above their 200-day average, confirming weak underlying trend depth.

Rates continue to constrain the system, with elevated rate volatility (MOVE ~84) limiting duration expansion and keeping financing conditions restrictive.

Volatility remains structurally elevated, with VIX at 23.9, alongside elevated VVIX (115) and SKEW (147) — confirming persistent demand for tail hedging.

Credit has stabilized, but remains structurally tight relative to baseline, reinforcing that capital conditions have not eased.

Globally, the system remains constrained, with the dollar holding near 100 and China down −7.1% YTD, signaling a lack of external confirmation.

There is no alignment strong enough to support expansion.

What Most Are Missing

Stabilization is being misinterpreted as improvement.

Credit has tightened over one week, but remains tighter than one month ago. Liquidity has increased, but has not translated into lower financing costs. Participation remains incomplete, and volatility remains priced.

Macro data reinforces the same divergence: payrolls printed +178K, while ISM Services fell to 49.8, signaling contraction alongside labor resilience.

The absence of stress is being mistaken for the presence of strength.

Why This Matters

Markets have moved through a clear sequence:

Stabilization

Volatility repricing

Active de-risking

Now: Controlled stabilization under constraint

At this stage, markets are no longer driven by earnings expansion or growth expectations. They are driven by financial conditions — specifically the interaction between credit, liquidity, and volatility.

Markets are no longer reacting to growth — they are reacting to conditions.

Forward Market Framework

Markets are approaching a decision point defined by financial conditions.

Liquidity begins to transmit into spreads and participation → Expansion driven by improved capital availability

Downside Scenario

Credit spreads widen from current levels

Dollar strengthens above ~100–102

Volatility re-accelerates across assets → Transition from stabilization into active de-risking

The next move will be determined by conditions — not price.

Bottom Line

Markets remain structurally intact, but constrained.

Institutional capital is:

Maintaining exposure

Holding hedges

Waiting for confirmation from credit and liquidity

Markets are not breaking — they are waiting for conditions to change.

Access the Full Institutional Report

The full VMSI report — including factor-level breakdowns, regime probabilities, and forward positioning signals used by institutional allocators — will be available upon relaunch.

The VICA platform relaunches mid-April 2026.

VICA Partners Research

About the VICA Institutional Market Sentiment Index (VMSI) The VMSI is VICA Research’s proprietary sentiment gauge designed to track shifts in institutional risk behavior, capital flow posture, and macro-driven volatility signals.

Each weekly score reflects a multi-factor model that incorporates a blend of market structure, flow dynamics, defensive rotation, and volatility hedging — calibrated against key technical and behavioral thresholds.

Index scale: 0–25: Critical Risk Zone 26–49: Defensive 50–74: Cautionary Optimism 75–100: Expansion / High Confidence

Unlike retail-facing indicators, VMSI is engineered for tactical allocation and capital positioning — not emotion or media headlines. VICA publishes the index weekly to offer a forward-focused lens on institutional sentiment and market inflection dynamics.

Important Notice

This report and the proprietary VICA Market Sentiment Index (VMSI) are confidential works of authorship protected by intellectual property laws. Unauthorized reproduction, copying, redistribution, or use without express permission from VICA Research is strictly prohibited and monitored.

This material is for informational purposes only and does not constitute investment advice.

VICA Research

The VICA Research platform and VMSI dashboard will relaunch in April 2026, introducing expanded institutional data tools and cross-asset analytics.

Capital does not follow headlines. It follows structure.