Institutional synchronization improved this week beneath concentrated persistence structures. Participation breadth stabilized, but trust, duration confirmation, and redundancy quality remained incomplete beneath visible stability.

VMSI Snapshot

Metric

Score

Structural State

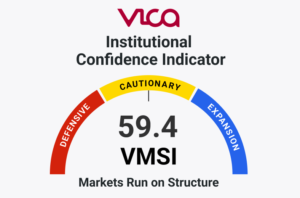

VMSI Composite

59.1

Stabilization exceeded normalization.

Momentum

64.0

Breadth improved beneath concentration.

Liquidity

59.8

Liquidity improved faster than confidence.

Volatility & Hedging

49.8

Hedging demand remained elevated.

Safe Haven Demand

50.9

Defensive positioning persisted.

Advanced Signal Layer

Framework

Score

Structural State

CMX

46.9

Convexity compression remained incomplete.

PDCS

72.4

Deployment broadened selectively.

GFP

60.8

Global propagation remained uneven.

PLMT

—

Structural compression persisted.

Executive Summary

The VMSI increased to 59.1 from 57.8 last week as breadth participation, liquidity diffusion, and deployment conditions stabilized beneath concentrated directional persistence.

However, the system still relied on concentrated liquidity leadership and elevated hedging persistence beneath visible calm.

The hidden pattern was clear:

Liquidity improved faster than institutional trust normalized.

That is the signal.

This remains a Structural Compression Stabilization regime, not a fully normalized expansion regime.

Market Structure

Participation breadth improved beneath concentrated liquidity leadership. Equal-weight participation stabilized relative to cap-weighted concentration while decentralized participation improved across value, real estate, and external participation structures.

Value participation remained strong, with VTV showing +19.13% 200-day period performance. VNQ confirmed real-asset participation repair with +8.07% 200-day period performance, while EEM showed +34.26% 200-day period performance. Those signals confirmed improving propagation breadth, but not full redundancy repair.

The Participation Integrity Coefficient improved as decentralized participation stabilized beneath concentrated leadership.

However, breadth improved without materially reducing concentration dependency.

That remains the market-structure signal institutional accounts should focus on.

Credit & Liquidity Conditions

Credit and liquidity conditions stabilized as institutional deployment broadened selectively beneath concentrated directional persistence.

HY OAS held at 2.78%, while IG OAS held at 0.75%, confirming that credit stress did not accelerate beneath improving participation conditions. Liquidity Diffusion Ratio conditions improved, while credit spread deterioration slowed relative to prior weeks. Dealer positioning remained volatility-suppressive, reinforcing operational stability beneath the surface.

However, liquidity improved faster than duration confidence.

Duration-sensitive structures remained incomplete. TLT, EDV, and ZROZ continued lagging broader participation repair, confirming that institutional trust did not normalize at the same rate as liquidity deployment.

That is the liquidity signal:

credit stabilized, but duration did not confirm full trust repair.

Positioning & Convexity

Volatility compressed tactically while institutional hedging persistence remained elevated beneath stable directional participation.

VIX closed at 16.70, while VVIX remained elevated near 91.16. SKEW held at 137.39, and MOVE closed at 78.43, confirming that realized volatility compressed faster than tail-risk and duration-risk pricing normalized.

The hidden pattern was not low volatility.

The hidden pattern was:

calm indexes masked unresolved hedging demand.

Convexity compression improved, but institutional protection behavior did not fully normalize. That matters because institutional accounts were willing to maintain directional exposure while keeping asymmetric protection active beneath the surface.

Equal-weight participation stabilized. Value synchronization strengthened. Real-estate participation improved. External participation repaired selectively. These signals confirmed that deployment broadened beyond the narrowest leadership channels.

However, technology-linked liquidity structures continued anchoring the system.

The Force Synchronization Coefficient improved as decentralized deployment stabilized beneath concentrated liquidity leadership.

But the key relationship remained:

deployment broadened without fully restoring redundancy quality.

That distinction matters for institutional funds because capital was moving back into the system, but the system still depended on concentrated force vectors to maintain stability.

Breadth participation improved while external propagation elasticity stabilized selectively across emerging-market and real-asset participation structures. Value and real-estate participation strengthened enough to confirm that internal propagation no longer deteriorated at last week’s pace.

However, technology-linked liquidity structures continued anchoring synchronization quality beneath broader participation stabilization.

The hidden pattern remained:

participation improved without fully restoring decentralized resilience.

This is why the current regime is stabilization, not expansion. Participation improved, but backup liquidity capacity remained incomplete.

Global Propagation Conditions

Global synchronization remained uneven despite improving domestic participation conditions.

Japan continued functioning as a stable propagation-confirmation layer, with EWJ showing +20.49% 200-day period performance. China remained the major fracture point, with FXI showing -6.01% 200-day period performance and remaining structurally weak beneath broader stabilization. DXY held near 99.24, reinforcing stable but uneven external liquidity conditions.

The global signal was clear:

external synchronization did not match domestic stabilization.

This matters because durable institutional expansion normally requires global propagation coherence. Current conditions showed selective external repair, not full global synchronization normalization.

Advanced Signal Layer

The dominant hidden-state transition was improving stabilization beneath ongoing structural compression.

Participation Dispersion Ratio conditions improved while Liquidity Diffusion Ratio conditions stabilized relative to prior deterioration phases. Propagation deterioration slowed, but convexity persistence and concentration dependency remained elevated beneath visible participation calm.

The VMSI signal was not simply that markets improved.

The signal was:

institutional stabilization improved faster than institutional trust normalized.

That is the pattern VMSI isolates.

This remains a Structural Compression Stabilization regime.

CMX — Convexity Metrics Index

CMX declined to 46.9, remaining inside a convexity persistence regime.

VVIX remained near 91, SKEW held near 137, and MOVE stabilized near 78. Those relationships confirmed that cross-asset hedging demand remained active even as realized volatility compressed.

The CMX signal was clear:

volatility compressed, but hedging behavior did not normalize.

That means fragility stabilized faster than institutional trust repaired. Directional exposure improved, but protection structures remained embedded.

Pre-Deployment Capital Signals (PDCS)

PDCS increased to 72.4, remaining inside a selective deployment expansion regime.

Liquidity diffusion improved while equal-weight breadth, value participation, and real-estate participation stabilized beneath concentrated directional persistence. Institutional deployment broadened materially relative to prior deterioration phases.

However, duration confirmation remained incomplete.

The PDCS signal was:

capital deployment improved faster than synchronization quality normalized.

That distinction matters because institutional capital began moving more broadly, but deployment still lacked full confirmation from duration, global propagation, and redundancy conditions.

GFP — Geopolitical Friction Pressure

GFP declined modestly to 60.8, remaining inside a structural friction regime.

Persistent dollar strength, weak China participation, and uneven emerging-market elasticity continued limiting broader global propagation coherence beneath improving domestic synchronization conditions.

Markets stabilized operationally.

However, the GFP signal remained:

global propagation stayed uneven beneath domestic stability.

Domestic participation repaired faster than global synchronization. That divergence remains important for institutional allocators because global transmission quality still failed to confirm full regime normalization.

Post-Linear Market Theory (PLMT)

One of the framework’s defining hidden-state principles remained visible this week:

stability itself can become structurally compressive.

Modern institutional liquidity systems increasingly reinforce passive concentration, mechanically reinforced participation, volatility suppression, reflexive deployment behavior, and synchronization persistence beneath visible stability.

But convexity persistence, incomplete participation redundancy, lagging duration confirmation, elevated concentration dependency, and uneven global synchronization remained embedded beneath stable headline participation.

The PLMT signal was:

stability improved, but resilience did not fully rebuild.

This remains Structural Compression Stabilization beneath visible calm.

Final Institutional Assessment

Institutional synchronization improved this week. Participation breadth stabilized, liquidity diffusion improved, and volatility compression normalized tactically beneath concentrated persistence structures.

However, structural normalization remained incomplete beneath visible stability.

Current conditions continue reflecting mechanically reinforced participation, incomplete propagation normalization, elevated hedging persistence, concentration dependency, and uneven global synchronization beneath stable headline participation.

This is not a deterioration regime.

It is stabilization beneath ongoing Structural Compression.

Stability improved. Compression persisted.

About the VICA Institutional Market Sentiment Index (VMSI)

The VICA Institutional Market Sentiment Index (VMSI) measures institutional risk across global markets through momentum, liquidity, volatility, credit, safe-haven demand, convexity dynamics, capital flow inertia, and geopolitical friction.

The model incorporates proprietary frameworks including CMX, PDCS, and GFP to identify state transitions in institutional behavior before they are fully reflected in price.

VMSI models markets as adaptive institutional systems where directional movement emerges through the synchronization, propagation, and interaction of capital flows, liquidity conditions, participation structures, and convexity positioning.

Unlike traditional sentiment frameworks, VMSI is engineered to identify hidden-state structural changes beneath headline market participation, including liquidity diffusion deterioration, convexity persistence, concentration dependency, propagation instability, and incomplete synchronization conditions.

Markets are analyzed in parts. VMSI™ measures the system.

Disclaimer

This report and the proprietary VICA Market Sentiment Index (VMSI) are confidential works of authorship protected by intellectual property laws. Unauthorized reproduction, copying, redistribution, or use without express permission from VICA Research is strictly prohibited and monitored.

This report is for informational purposes only and does not constitute investment advice or a recommendation. Views are based on current data and VICA Research models and are subject to change.