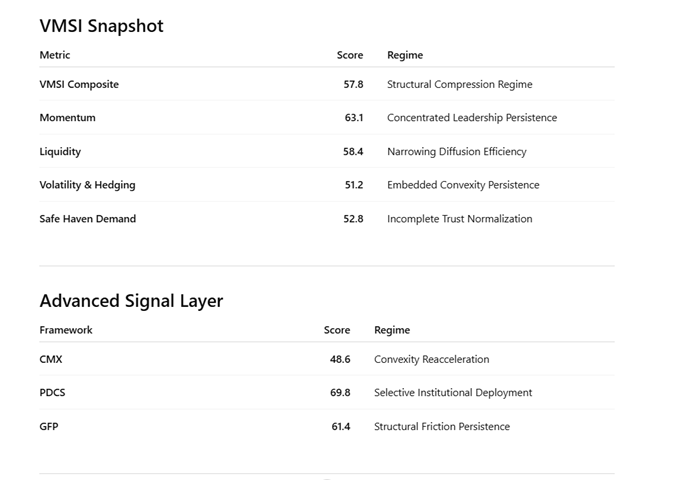

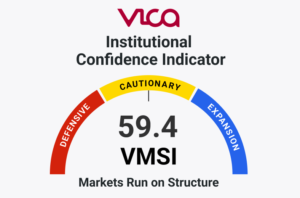

The VMSI declined to 57.8 this week as institutional synchronization quality weakened beneath stable cap-weighted participation.

That was the signal.

Most investors focused on stable index participation. Institutional capital focused on deteriorating propagation quality beneath the surface. Participation dispersion widened, liquidity concentration accelerated, duration confirmation weakened, and convexity persistence remained elevated simultaneously.

Institutional liquidity persisted before institutional trust normalized.

That distinction defined the regime.

The deterioration was measurable. The Participation Dispersion Ratio (PDR) widened approximately 340bps week-over-week, while the Global Elasticity Coefficient (GEC) deteriorated as external participation elasticity weakened approximately 2.4x faster than concentrated domestic persistence.

At the same time:

the Liquidity Diffusion Ratio (LDR) deteriorated for the third consecutive week

the Credit Synchronization Ratio (CSR) flattened beneath stable directional participation

the VVIX/VIX Convexity Persistence Spread remained more than 4.8x above compression equilibrium

The most important structural development this week was not stable headline participation.

It was deteriorating synchronization beneath concentrated leadership persistence.

Participation propagation weakened while concentrated liquidity persistence remained stable. Breadth diffusion decelerated, equal-weight synchronization weakened, and participation redundancy deteriorated simultaneously beneath stable directional participation.

Approximately 63% of equities continue trading above intermediate participation structures, but propagation quality weakened materially underneath.

The deterioration was measurable. The Participation Integrity Coefficient (PIC) weakened for the fourth consecutive week as decentralized participation deteriorated approximately 1.9x faster than concentrated persistence normalized.

At the same time:

the Participation Dispersion Ratio (PDR) continued widening

cyclical participation elasticity softened

cross-factor synchronization weakened

propagation breadth decelerated

simultaneously.

That combination matters because durable institutional expansion normally requires decentralized propagation reinforcement.

Credit and liquidity synchronization weakened this week.

That matters because institutional deployment rarely remains durable when credit acceleration fails confirmation beneath directional participation persistence.

The deterioration was measurable. The Credit Synchronization Ratio (CSR) weakened as spread-compression acceleration decelerated beneath stable concentrated participation.

At the same time:

the Duration Trust Divergence Ratio (DTDR) widened as duration-sensitive participation weakened approximately 1.7x faster than concentrated participation persistence

the Liquidity Diffusion Ratio (LDR) continued deteriorating

cross-asset propagation coherence weakened

simultaneously.

That combination matters because durable institutional expansion normally requires synchronized reinforcement across:

Last week, institutional deployment broadened across participation systems.

This week, deployment re-concentrated into dominant liquidity channels.

The transition was measurable. The Liquidity Diffusion Ratio (LDR) deteriorated for the third consecutive week as concentrated persistence exceeded decentralized propagation capacity by approximately 2.7:1, while the Participation Dispersion Ratio (PDR) widened approximately 340bps week-over-week simultaneously.

At the same time:

the Global Elasticity Coefficient (GEC) deteriorated as external participation elasticity weakened approximately 2.4x faster than domestic concentrated persistence

the Participation Integrity Coefficient (PIC) weakened for the fourth consecutive week

the Credit Synchronization Ratio (CSR) flattened beneath stable directional participation

But deployment quality weakened beneath stable surface participation.

Positioning & Hedging

Positioning behavior continued revealing the divergence between participation and conviction.

Directional participation remained stable, but institutional protection demand failed normalization proportionally with surface participation conditions.

That divergence remained measurable.

The VVIX/VIX Convexity Persistence Spread remained more than 4.8x above historical compression equilibrium, while the Convexity Persistence Ratio (CPR) remained elevated simultaneously beneath stable directional participation.

At the same time:

the Duration Trust Divergence Ratio (DTDR) widened materially

convexity compression failed normalization

institutional asymmetry demand remained elevated

cross-asset hedging persistence remained embedded

simultaneously.

That combination confirmed institutions continued maintaining:

The dominant transition this week was deteriorating institutional synchronization beneath stable directional participation.

That is the signal most frameworks still fail to isolate.

Last week’s regime reflected improving transmission:

tightening credit

expanding breadth

improving participation diffusion

stabilizing volatility transmission

strengthening propagation efficiency

This week, the structure changed.

Participation dispersion widened. Duration confirmation weakened. Convexity persistence remained elevated. Global liquidity elasticity softened. Propagation efficiency deteriorated simultaneously.

The deterioration was measurable. The Force Synchronization Coefficient (FSC) weakened as the Participation Dispersion Ratio (PDR) widened approximately 340bps week-over-week, while the Global Elasticity Coefficient (GEC) deteriorated as external participation elasticity weakened approximately 2.4x faster than concentrated domestic persistence.

At the same time:

the Liquidity Diffusion Ratio (LDR) deteriorated for the third consecutive week

the Duration Trust Divergence Ratio (DTDR) widened materially

the VVIX/VIX Convexity Persistence Spread remained structurally above equilibrium

Institutional capital is no longer broadening transmission at the same rate.

It is selectively concentrating deployment again.

This is not instability.

It is:

structural compression through synchronization decay.

CMX — Convexity Metrics Index

CMX increased to 48.6 / 100, remaining inside a convexity persistence regime.

The increase was driven by embedded asymmetry demand beneath stable participation conditions.

The deterioration was measurable. The Convexity Persistence Ratio (CPR) remained elevated while the VVIX/VIX Convexity Persistence Spread remained more than 4.8x above equilibrium, confirming convexity demand failed normalization despite stable directional participation.

At the same time:

cross-asset hedging persistence remained elevated

duration confirmation weakened

convexity compression failed normalization

institutional asymmetry demand remained embedded

simultaneously.

Fragility stabilized faster than trust normalized.

That distinction continues defining the current convexity regime.

Pre-Deployment Capital Signals (PDCS)

PDCS declined to 69.8 / 100, remaining inside a selective deployment regime.

Last week, institutional deployment broadened across participation systems.

This week, deployment selectively re-concentrated.

The deterioration was measurable. The Propagation Efficiency Differential (PED) weakened as concentrated liquidity persistence increasingly exceeded decentralized propagation capacity, while the Participation Integrity Coefficient (PIC) weakened for the fourth consecutive week as decentralized participation deteriorated approximately 1.9x faster than concentrated persistence normalized.

At the same time:

the Liquidity Diffusion Ratio (LDR) deteriorated approximately 2.7:1 in favor of concentrated persistence over decentralized propagation

the Credit Synchronization Ratio (CSR) weakened beneath stable directional participation

the Global Elasticity Coefficient (GEC) deteriorated alongside weakening external participation elasticity

simultaneously.

These are not instability conditions.

They are selective deployment conditions.

Capital remains active ahead of conviction normalization.

That remains the defining asymmetry inside the current regime.

GFP — Geopolitical Friction Pressure

GFP increased to 61.4 / 100, placing the system inside a structural friction regime.

The most important feature of the current regime is not geopolitical instability.

It is embedded geopolitical distrust beneath stable participation conditions.

The deterioration was measurable. The Global Elasticity Coefficient (GEC) weakened as external participation elasticity deteriorated approximately 2.4x faster than concentrated domestic persistence, confirming external liquidity synchronization weakened beneath stable internal participation conditions.

At the same time:

institutional hedging persistence remained elevated

Institutions focus on how synchronization quality is behaving beneath the market.

That is the difference.

This week’s signal was not stable prices. The signal was simultaneous deterioration in:

participation diffusion

propagation efficiency

duration confirmation

external liquidity elasticity

convexity normalization

while concentrated persistence remained stable beneath the surface.

The deterioration was measurable. The Force Synchronization Coefficient (FSC) weakened as the Participation Dispersion Ratio (PDR) widened approximately 340bps week-over-week, while the Liquidity Diffusion Ratio (LDR) deteriorated for the third consecutive week and the Global Elasticity Coefficient (GEC) weakened as external participation elasticity deteriorated approximately 2.4x faster than concentrated domestic persistence.

More importantly, the system began exhibiting:

asymmetric propagation behavior.

Directional persistence remained stable, but decentralized participation propagation decelerated materially beneath concentrated liquidity reinforcement. Historically, that pattern appears when institutional deployment continues operating ahead of full conviction normalization.

At the same time:

the VVIX/VIX Convexity Persistence Spread remained structurally above equilibrium

the Duration Trust Divergence Ratio (DTDR) continued widening

structural compression through synchronization decay.

Not collapse.

The system remains operationally stable, but force coherence weakened materially beneath headline participation.

Institutional capital continues deploying before institutional conviction fully normalizes.

That is the hidden pattern inside this week’s data.

Bottom Line

The VMSI declined to 57.8 because institutional liquidity continued concentrating while participation synchronization weakened beneath the surface.

That was the real signal.

The deterioration was measurable:

the Participation Dispersion Ratio (PDR) widened approximately 340bps week-over-week

the Liquidity Diffusion Ratio (LDR) deteriorated for the third consecutive week

external participation elasticity weakened approximately 2.4x faster than concentrated domestic persistence

duration-sensitive participation weakened approximately 1.7x faster than concentrated equity persistence

simultaneously.

At the same time, convexity normalization failed. The VVIX/VIX Convexity Persistence Spread remained structurally above equilibrium while credit synchronization flattened beneath stable directional participation.

That combination confirms:

liquidity persisted faster than institutional trust normalized.

But propagation quality, participation breadth, and synchronization coherence weakened materially underneath.

The rally continued.

The system didn’t.

About the VICA Institutional Market Sentiment Index (VMSI)

The VICA Institutional Market Sentiment Index (VMSI) measures institutional risk across global markets through momentum, liquidity, volatility, credit, safe-haven demand, convexity dynamics, capital flow inertia, and geopolitical friction.

The model incorporates proprietary frameworks including CMX, PDCS, and GFP to identify state transitions in institutional behavior before they are fully reflected in price.

VMSI models markets as adaptive institutional systems where directional movement emerges through the synchronization, propagation, and interaction of capital flows, liquidity conditions, participation structures, and convexity positioning.

Markets are analyzed in parts. VMSI™ measures the system.

Disclaimer

This report is for informational purposes only and does not constitute investment advice or a recommendation. Views are based on current data and VICA Research models and are subject to change.

This report and the proprietary VICA Institutional Market Sentiment Index (VMSI) are protected intellectual property. Unauthorized reproduction, redistribution, or use without express permission from VICA Research is prohibited.

VICA Research

Capital does not follow headlines. It follows structure.