Participation Strengthened. Caution Remained Warranted.

July 6, 2026

Matthew Krumholz

Week Ending July 3, 2026

Institutional market conditions improved as participation broadened, credit remained orderly, and capital deployment continued across core allocation channels. Caution remained warranted as technology weakness, elevated tail-risk hedging, and uneven global participation continued to limit a fully confirmed institutional expansion.

Live Report: vicapartners.com

VMSI™ Snapshot

Framework

Score

Institutional State

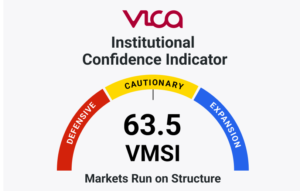

VMSI Composite

65.2

Institutional conditions improved modestly as participation broadened while conviction remained selective.

Momentum

69.7

Market participation expanded beyond narrow leadership despite continued technology weakness.

Liquidity

62.7

Liquidity conditions strengthened as credit markets remained orderly and institutional capital deployment continued.

Volatility & Hedging

60.8

Hedging demand continued to normalize, although institutional risk management remained active.

Safe Haven Demand

48.2

Defensive positioning continued to ease as capital rotated incrementally toward risk assets.

Advanced Framework Layer

Framework

Score

Institutional State

SPI™

68.4

Participation broadened across the market, supporting improved structural integrity beneath headline performance.

CMX™

60.1

Convexity pressures continued to ease, although institutional hedging remained above fully normalized levels.

PDCS™

72.1

Institutional capital deployment remained constructive, with participation extending beyond the narrowest areas of leadership.

GFP™

66.2

Global participation improved overall but remained uneven as regional leadership continued to diverge.

PLMT™

Selective Synchronization Expansion

Market structure continued to strengthen, although confirmation remained incomplete across sectors, asset classes, and global markets.

IC-VMSI™

69.6

Institutional accumulation remained constructive as core passive and benchmark-driven capital continued supporting overall market structure.

Executive Summary

The VMSI™ Composite increased to 65.2 from 64.0, reflecting another week of improving institutional market conditions. Momentum rose to 69.7, Liquidity improved to 62.7, and Volatility & Hedging advanced to 60.8, indicating the improvement remained supported by expanding participation and orderly market conditions rather than a single risk-on impulse.

Participation continued broadening while credit conditions remained supportive and institutional capital deployment stayed constructive. SPI increased to 68.4, PDCS advanced to 72.1, and IC-VMSI improved to 69.6, indicating stronger coordination across market structure, institutional deployment, and benchmark-driven capital flows.

The improvement remained measured rather than complete. Safe Haven Demand declined to 48.2, while CMX improved to 60.1 and GFP increased to 66.2, indicating that institutional confirmation continued strengthening despite persistent technology weakness, China divergence, and elevated tail-risk hedging.

Taken together, independent measures of market structure, liquidity, credit conditions, positioning, and institutional deployment supported the same conclusion. VMSI therefore maintains the Selective Synchronization Expansion regime, reflecting improving institutional conditions while broader market confirmation remains incomplete.

Key Takeaway: Institutional participation continued strengthening beneath the surface, but broader market confirmation remains necessary before the current expansion can be considered fully synchronized.

Market Structure

Institutional participation continued broadening as market structure strengthened beneath the surface. The Participation Integrity Ratio (PIR™ = RSP ÷ SPY) remained consistent with expanding participation, indicating equal-weight stocks continued supporting capitalization-weighted index performance despite modest weakness in large-cap technology.

Market breadth remained constructive across sectors and market capitalizations. Although headline index gains were supported by large-cap benchmarks, value continued outperforming growth and broader participation remained supportive, indicating that underlying institutional activity remained healthier than index performance alone suggested.

Confirmation, however, remained incomplete. Technology leadership weakened, China continued diverging from other international markets, and elevated tail-risk hedging indicated institutional investors maintained disciplined positioning despite improving participation.

Taken together, PIR™, improving breadth, orderly credit conditions, and broader participation indicate institutional market structure continued strengthening, although full confirmation across leadership and global participation has yet to emerge.

Structural Conclusion: Participation strengthened faster than institutional confirmation.

Credit & Liquidity Conditions

Credit conditions remained orderly as institutional funding markets continued functioning without evidence of systemic stress. The Credit Quality Ratio (CQR™ = LQD ÷ HYG) remained stable, while both investment-grade and high-yield credit continued trading within contained ranges despite modest week-to-week divergence.

Investment-grade credit continued showing stronger sponsorship than high yield. LQD closed at 108.64 while HYG finished at 79.71, producing a CQR™ of 1.363, indicating institutional preference continued favoring higher-quality credit without a broad withdrawal from corporate credit markets.

Credit spread acceleration remained contained. HY OAS and IG OAS showed only modest week-to-week movement, suggesting recent market volatility reflected tactical portfolio adjustments rather than deterioration in underlying credit quality or institutional funding conditions.

Taken together, stable CQR™, contained credit spreads, and orderly corporate credit trading indicate liquidity conditions continued supporting broader institutional market coordination.

Structural Conclusion: Credit quality remained stronger than institutional risk aversion.

Positioning & Convexity

Institutional positioning continued normalizing as hedging activity remained disciplined rather than defensive. The Hedging Preference Ratio (HPR™ = CPCE ÷ CPCI) remained consistent with portfolio-level hedging exceeding single-stock hedging, indicating institutions continued managing portfolio risk without signaling broad market stress.

Dealer positioning became modestly more supportive as the Convexity Management Index (CMX™) improved to 60.1. Although implied volatility continued stabilizing, elevated tail-risk pricing indicated institutional investors maintained downside protection despite improving market participation.

ETF flow data reinforced this positioning. Equity allocations remained constructive while bond allocations stabilized, indicating institutions continued reallocating capital within portfolios rather than materially reducing overall market exposure.

Taken together, HPR™, improving convexity conditions, and constructive ETF flows indicate institutions continued managing risk through selective positioning rather than broad de-risking.

Structural Conclusion: Institutional positioning remained constructive as hedging became increasingly selective.

Flow & Allocation Behavior

Institutional capital continued deploying across markets despite selective leadership and ongoing regional divergence. The Deployment Force Ratio (DFR™ = Equity ETF Flows ÷ Bond ETF Flows) indicated allocation behavior remained constructive, though more balanced between equity exposure and fixed income than in prior weeks.

Rather than evaluating equity and bond flows independently, DFR™ transforms those observations into a measure of institutional allocation preference. Equity allocations remained positive in aggregate, while bond demand also remained supportive, indicating benchmark-linked capital continued participating in risk assets while preserving portfolio balance.

This week’s allocation patterns remained consistent with constructive institutional positioning. Core benchmark-linked equity exposure remained supported, while bond allocations continued stabilizing, indicating portfolio reallocation rather than broad defensive repositioning.

Taken together, DFR™, IC-VMSI™, and ETF flow behavior indicate institutional capital continued deploying across risk assets while maintaining disciplined portfolio diversification.

Structural Conclusion: Capital deployment favored risk assets without eliminating portfolio balance.

Global Propagation Conditions

Global participation remained constructive but uneven across regions. The Global Propagation Ratio (GPR™ = VEA ÷ VWO) remained consistent with stronger institutional sponsorship of developed markets, indicating global participation continued broadening selectively rather than uniformly.

Rather than evaluating international markets independently, GPR™ transforms regional performance into a measure of institutional capital propagation. Developed markets remained more resilient than emerging markets, while China continued lagging broader global participation.

Supporting market evidence reinforced this interpretation. VEA finished at 70.81 and VWO at 59.04, producing a GPR™ of approximately 1.20. EFA remained constructive, EWJ stayed resilient, while EEM, IEMG, and FXI reflected weaker emerging-market participation. A firmer U.S. dollar also continued creating headwinds for parts of the emerging-market complex.

Taken together, GPR™, GFP, and global allocation behavior indicate institutional capital continued propagating across global markets while maintaining a preference for developed-market quality and selective regional deployment.

Structural Conclusion: Global participation remained constructive, but institutional deployment stayed selective.

Advanced Signal Layer

Independent structural measures continued converging on the same institutional conclusion. SPI, CMX, PDCS, GFP, and IC-VMSI each measured different dimensions of market behavior, yet collectively identified improving institutional conditions without confirming a fully synchronized expansion.

Rather than evaluating these measures independently, the Advanced Signal Layer integrates information relationships, pattern recognition, hidden-state estimation, and independent signal confirmation. The convergence of multiple frameworks provides greater confidence that observed conditions reflect underlying market structure rather than short-term market noise.

This week’s evidence remained internally consistent. SPI confirmed stronger participation integrity, CMX indicated improving but incomplete convexity conditions, PDCS confirmed continued institutional capital deployment, GFP supported selective global propagation, and IC-VMSI reinforced sustained benchmark-linked institutional buying.

Taken together, the Advanced Signal Layer indicates that improving institutional conditions are supported by multiple independent sources of evidence rather than any single market indicator.

Structural Conclusion: Independent structural signals strengthened together, but full institutional confirmation remained incomplete.

Structural Discoveries

1. Participation improved faster than institutional confirmation. Broader market participation strengthened as SPI advanced, but technology weakness, elevated tail-risk positioning, and uneven global participation prevented full institutional confirmation.

2. Credit continued validating capital deployment. Stable credit conditions, contained spread behavior, and orderly liquidity confirmed institutions continued allocating capital without evidence of systemic funding stress.

3. Independent structural signals strengthened together. The Advanced Signal Layer independently confirmed improving participation, liquidity, positioning, deployment, and global propagation, reinforcing the Selective Synchronization Expansion regime.

Structural Assessment: Independent information relationships and structural validation frameworks converged on the same institutional regime with high confidence, supporting continued improvement while maintaining a disciplined level of caution.

Final Institutional Assessment

The independent evidence presented throughout this report converged on the same institutional conclusion. Participation strengthened, credit conditions remained orderly, capital deployment continued expanding, and global participation remained constructive but uneven, while institutional confirmation remained incomplete.

The VMSI™ framework reached this conclusion through a structured sequence of observation, information extraction, pattern recognition, hidden-state estimation, and independent signal confirmation. Proprietary relationship metrics (PIR™, CQR™, HPR™, DFR™, and GPR™) transformed observable market conditions into institutional information, while the Advanced Signal Layer independently validated the resulting structural assessment.

Collectively, the evidence indicates that institutional market organization continued improving without evidence of systemic deterioration. Orderly liquidity, stable credit conditions, disciplined capital deployment, and broader participation supported further improvement, while technology weakness, China divergence, and elevated tail-risk positioning continued to justify a measured level of caution.

Regime Assessment: The institutional market regime remains Selective Synchronization Expansion, characterized by improving market organization, constructive capital deployment, broader participation, and selective institutional confirmation.

About the VICA Institutional Market Sentiment Index (VMSI™)

The VICA Institutional Market Sentiment Index (VMSI™) is an observational market framework that measures the institutional conditions shaping market behavior before those conditions become fully reflected in prices.

Rather than analyzing individual indicators in isolation, VMSI measures the relationships among participation, liquidity, credit, positioning, capital deployment, and global propagation to identify the underlying organization of institutional markets.

Each weekly publication integrates observable market data, proprietary relationship metrics, and independent structural validation to estimate the current institutional market regime.

IC-VMSI™ (Institutional Capital VMSI) measures institutional capital deployment through ownership, allocation, portfolio positioning, and benchmark-linked investment behavior. The framework estimates institutional capital deployment across markets using observable evidence rather than individual trade reporting.

Disclaimer

VMSI™ is a proprietary observational market framework developed by VICA Research. This publication is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Conclusions reflect evidence-based interpretations of available market information at the time of publication and may change as new evidence becomes available.

Participation broadened across domestic and global markets as institutional deployment, credit conditions, and global propagation improved. Confidence remained incomplete as...

Participation broadened across domestic and global markets as institutional deployment improved and volatility conditions stabilized. Resilience remained incomplete as leadership...

Credit conditions held while institutional protection demand expanded. Participation, duration confirmation, and global propagation remained incomplete beneath the hedging response....