Structural Mechanics And Post-Linear Market Theory

May 21, 2026

Matthew Krumholz

Why Modern Market Structure Increasingly Distorts Informational Purity

Abstract

Classical financial theory largely modeled markets as equilibrium systems governed through information discovery, valuation adjustment, and decentralized participation.

Modern financial systems increasingly behave differently.

Across equities, rates, derivatives, and cross-asset liquidity systems, market behavior increasingly reflects liquidity transmission, passive concentration, volatility response, reflexive positioning, and capital synchronization operating simultaneously across interconnected structures.

Post-Linear Market Theory proposes that modern markets increasingly behave as adaptive liquidity systems rather than isolated valuation mechanisms.

Under this framework, price increasingly emerges from interacting structural conditions operating beneath visible market narratives.

As market structure evolves, the relationship between price, participation, volatility, and informational integrity evolves with it.

I. The Structural Shift

Classical finance assumed that price broadly reflected information, volatility broadly reflected risk, and capital allocation broadly followed productive economic expectations.

For decades, these assumptions functioned reasonably well.

The issue today is not that classical finance was incorrect. The issue is that modern financial systems increasingly operate under structural conditions those frameworks were never designed to interpret.

Over the last fifteen years, passive ownership, derivatives activity, volatility-targeting systems, benchmark concentration, and systematic liquidity behavior increasingly became dominant drivers of market behavior.

As a result, price increasingly reflects liquidity architecture itself rather than independent economic conviction alone.

Modern markets increasingly behave less like equilibrium systems and more like adaptive liquidity ecosystems governed through propagation, synchronization, and reflexive reinforcement.

Contemporary Example: AI Concentration

Recent AI-driven market leadership increasingly illustrates this transition.

Public interpretation frequently centers around innovation, productivity expansion, and earnings acceleration. Beneath the surface, however, market behavior increasingly reflects benchmark reinforcement, passive allocation mechanics, liquidity concentration, and synchronized institutional participation.

As benchmark-heavy leaders appreciate, passive inflows mechanically allocate additional capital toward those same liquidity centers. Price appreciation itself increasingly reinforces additional participation.

Capital movement increasingly influences future capital movement.

II. Stability Now Masks Fragility

One of the defining characteristics of modern market structure is that stability itself increasingly contributes to hidden fragility.

When volatility remains suppressed, systematic exposure expands, passive flows reinforce concentration, liquidity dependency deepens, and positioning becomes increasingly crowded.

This creates the appearance of resilience while weakening structural flexibility beneath the surface.

Under post-linear conditions, fragility frequently accumulates during periods of apparent calm.

Structural instability often compounds invisibly during periods of perceived equilibrium.

Contemporary Example: Volatility Compression

Extended low-volatility environments increasingly demonstrated these conditions.

As realized volatility declined, volatility-targeting systems and risk-controlled mandates mechanically expanded exposure. Increased participation itself then contributed to further volatility suppression, reinforcing additional positioning expansion.

Stability increasingly became dependent upon continued structural participation.

Volatility no longer functioned purely as a passive measure of risk. Volatility increasingly became an active transmission variable governing leverage capacity and participation behavior throughout the system.

Observed stability can simultaneously increase latent systemic fragility beneath the surface.

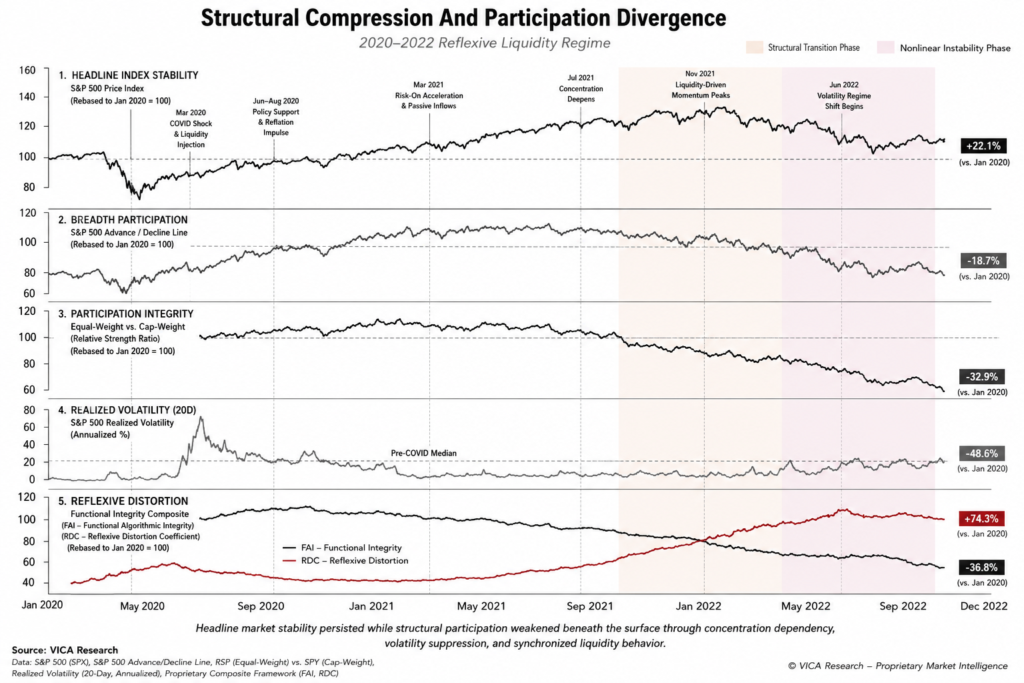

Structural Compression And Participation Divergence

2020–2022 Reflexive Liquidity Regime

This framework illustrates one of the central observations underlying Post-Linear Market Theory:

Headline market stability can persist while structural participation deteriorates beneath the surface.

Between 2020 and 2022, index-level resilience increasingly diverged from broader participation quality. Breadth weakened, concentration dependency accelerated, volatility remained structurally compressed, and reflexive liquidity behavior increasingly reinforced benchmark-heavy leadership.

Under traditional market assumptions, price strength was generally interpreted as evidence of broad participation and improving informational integrity.

Under post-linear conditions, price increasingly reflects liquidity architecture interacting with itself through passive concentration, synchronized positioning, and volatility-dependent participation behavior.

The chart illustrates how apparent market stability can coexist with increasing structural fragility operating beneath the surface.

This divergence represents one of the foundational observations supporting Post-Linear Market Theory.

III. Informational Purity And Reflexive Liquidity

Traditional market analysis relies heavily on comparative relationships.

Historically, relative strength was interpreted as evidence of institutional conviction and improving participation quality.

Modern market structure increasingly distorts those signals.

Relative outperformance can increasingly reflect passive inclusion mechanics, liquidity concentration, volatility suppression, and positioning persistence rather than broad structural expansion.

Markets can appear strongest precisely when participation quality is deteriorating internally.

Mainstream financial interpretation increasingly reflects this transition. Market discussion now frequently centers around flows, positioning, concentration, liquidity sensitivity, and volatility response.

These observations are important.

However, they often represent surface-level descriptions of deeper structural interactions operating beneath modern financial systems.

Contemporary Example: Narrowing Participation

This dynamic became increasingly visible prior to the 2022 market reversal.

Headline indices remained resilient while breadth weakened, equal-weight participation deteriorated, concentration dependency accelerated, and volatility sensitivity quietly compounded beneath the surface.

The deeper issue was not volatility alone.

The deeper issue was that market structure increasingly optimized for stability appearance rather than structural resilience itself.

IV. The Collapse Of Independent Price Discovery

Modern financial systems increasingly behave as synchronized liquidity systems.

Historically, securities responded more independently to company fundamentals, earnings expectations, valuation differences, and decentralized institutional allocation.

Today, correlations increasingly converge regardless of underlying economic differences.

Securities with materially different characteristics increasingly move together as components of the same liquidity architecture.

This increasingly reflects passive index flows, ETF mechanics, volatility-targeting systems, derivatives hedging flows, and systematic de-risking behavior operating simultaneously across interconnected systems.

Under these conditions, liquidity itself increasingly becomes the dominant short-term transmission variable.

Contemporary Example: Sovereign Bond Instability

Recent sovereign bond volatility increasingly reflects these conditions.

Public interpretation frequently attributes these moves to inflation expectations or central bank policy shifts alone. However, recent bond market behavior increasingly exhibits characteristics associated with transmission instability across interconnected positioning structures.

Even modest shifts in liquidity conditions or duration expectations increasingly generate outsized reactions simultaneously across sovereign rates, currencies, equities, and credit markets.

These reactions increasingly reflect synchronized liquidity systems operating beneath visible macroeconomic interpretation.

V. Reflexive Synchronization And Structural Compression

As passive concentration and liquidity synchronization expand, markets increasingly compress informational differentiation across assets.

This can temporarily reinforce stability while weakening decentralized price discovery.

Under post-linear conditions, persistence should not automatically be confused with systemic strength.

A system can continue functioning while simultaneously becoming increasingly fragile beneath the surface.

The more synchronized modern markets become, the more structurally dependent stability itself may become.

The continued expansion of passive allocation increasingly demonstrates structural compression dynamics.

As passive capital expands, larger benchmark constituents receive mechanically larger inflows independent of valuation dispersion or participation quality.

Participation increasingly synchronizes around common liquidity centers.

This can suppress dispersion temporarily while simultaneously increasing concentration dependency throughout the broader system.

Resilience increasingly depends upon continued flow persistence itself.

VI. The VMSI Structural Framework

The VMSI framework was developed around a central premise:

Modern markets must increasingly be analyzed through liquidity behavior, participation integrity, volatility structure, concentration dynamics, and reflexive reinforcement systems.

Traditional frameworks primarily measure price movement.

VMSI attempts to measure the structural quality of participation driving price behavior beneath the surface.

The objective is not merely to identify movement.

The objective is to determine whether market behavior reflects genuine structural expansion or mechanically reinforced stability generated through concentrated liquidity systems.

To operationalize this framework, VICA Research developed VMSI, SPIS, SPFI, FAI, and RDC to evaluate structural participation quality, informational integrity, reflexive distortion, and liquidity dependency operating throughout modern financial systems.

Conclusion

Modern financial markets increasingly behave as adaptive liquidity systems shaped through reflexivity, concentration, positioning dynamics, volatility response, and self-reinforcing participation behavior.

As a result, comparative price movement alone is becoming less reliable as a standalone measure of structural health.

Markets can remain elevated while participation weakens internally. Stability can persist while fragility compounds beneath the surface. Relative strength can improve while informational purity deteriorates.

Under post-linear conditions, stability itself increasingly becomes the mechanism through which fragility accumulates.

Post-Linear Market Theory represents an attempt to evolve institutional market analysis beyond equilibrium-based interpretation toward a structural understanding of adaptive liquidity systems.

The deepest risks and opportunities increasingly emerge not from observable price behavior alone, but from the structural forces shaping participation underneath it.

About The VICA Institutional Market Sentiment Index

The VICA Institutional Market Sentiment Index is VICA Research’s proprietary framework for evaluating structural participation, liquidity behavior, volatility conditions, behavioral persistence, and capital durability beneath headline market movement.

Unlike traditional sentiment models focused primarily on price direction, VMSI emphasizes the integrity, quality, and psychology of participation driving the market itself.

Markets are often analyzed in parts.

VMSI studies the system.

Disclaimer

This material is intended for research and informational purposes only and should not be interpreted as investment advice, a recommendation, or a prediction of future market outcomes.

Post-Linear Market Theory represents a structural research framework designed to study liquidity behavior, participation dynamics, and market system interactions.

Understanding the Gap Between Headlines and Market Structure Modern markets are increasingly driven by structure, liquidity, positioning, and systems behavior...

Why Modern Market Structure Increasingly Distorts Informational Purity A Structural Reassessment of Reflexive Liquidity, Signal Integrity, and Adaptive Capital Systems...

Executive Thesis Financial markets continue to evaluate geopolitical instability through an increasingly outdated framework. Most institutional models remain event-based: conflict...