VMSI REPORT

Executive Briefing

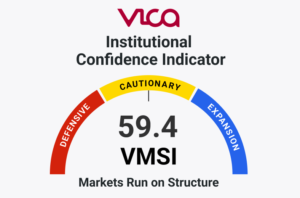

Markets have entered an early-stage de-risking phase beneath a stable index surface. The VICA Institutional Market Sentiment Index (VMSI) declined to 53.6, reflecting a shift from balanced positioning toward incremental risk reduction.

The defining signal this week is the breakdown in momentum (49.9) below neutral thresholds, combined with elevated volatility (VIX ~26.9) and a sharp expansion in rate volatility (MOVE +28%). This configuration confirms that institutional capital is transitioning from passive exposure to active risk management.

Importantly, credit markets remain stable, indicating that current conditions reflect repositioning and de-grossing rather than systemic stress or forced liquidation.

Cross-Asset Mechanics

- Equities: Broad-based momentum deterioration across all major indices, with price action breaking below short-term and intermediate trend structures

- Rates: Rising yield volatility driving duration compression and valuation instability

- Volatility: Persistent hedging demand with early signs of cross-asset transmission

- Credit: Controlled spread widening, signaling stability in funding conditions

This alignment indicates that risk is being reduced through positioning adjustments, not liquidity breakdowns.

Regime Interpretation

The current environment reflects a policy-driven market regime, where:

- Rate volatility is the primary transmission channel

- Equity weakness is a function of multiple compression, not earnings collapse

- Institutional flows are defensive but orderly

Historically, this structure precedes downside-biased consolidation with elevated volatility, rather than immediate systemic risk escalation.

Key Signal

Neutral Market. Defensive Capital.

Momentum breakdown + elevated volatility confirms a transition toward active institutional de-risking, with forward direction dependent on rate stabilization and Federal Reserve signaling.

Bottom Line

Markets remain structurally stable, but internally weaker.

Institutional capital is reducing exposure at the margin, increasing sensitivity to macro shocks.

The next phase will be determined by whether:

- Rate volatility stabilizes → consolidation

- Rate volatility expands → accelerated downside repricing